Credit Report VS Credit Score

Understanding your credit report and how your credit score can impact small business loans is a crucial aspect of your small business.

-

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

-

REVIEWED BY

Expert Contributor

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

Key Takeaway

A credit report offers detailed information about your credit history, and it is useful for long-term planning and loan applications, where a credit score provides a general snapshot of your creditworthiness, and is often used by lenders to assess loan applications.

Whether you need to know for a small business loan application, personal use, or general management of your business, it’s important to understand how credit reports and credit scores differ.

Table of Contents

What Is The Difference Between A Credit Report & A Credit Score?

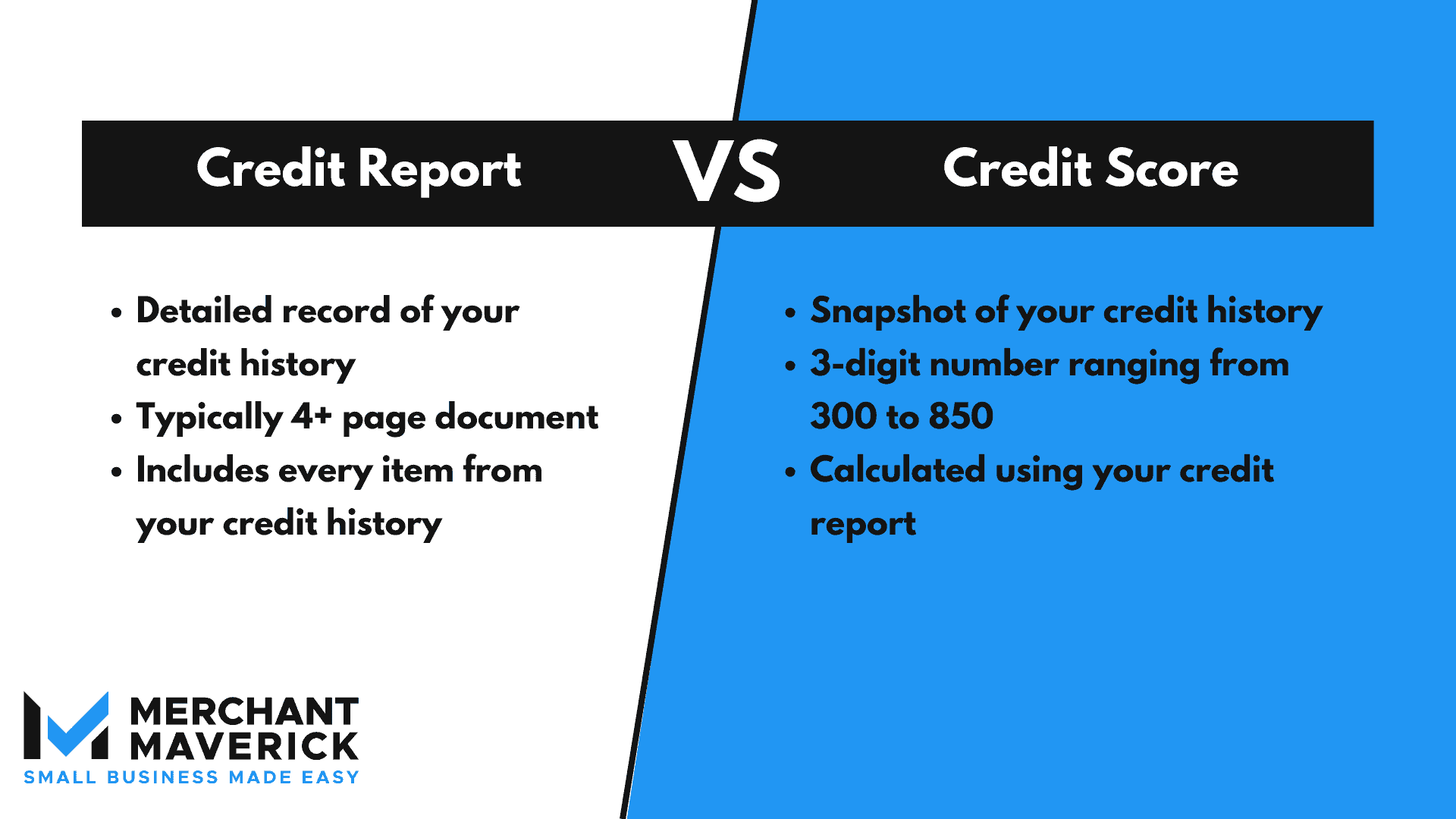

Your credit report is going to provide detailed information about your credit history, while your credit score provides a much more general snapshot of your current credit standing. You can use any credit bureau to receive a credit report, but the main three are Experian, TransUnion, and Equifax.

Some lenders will refer to a credit report more generally as your credit history. So, if you are asked to provide your credit history versus your credit score, you’ll want to use a credit bureau to obtain an up-to-date credit report.

Understanding Your Credit Report

On a credit report, you’ll see detailed information about your credit history.

A typical credit report will give you a full breakdown of all your open or closed credit accounts, bank accounts, loans, and payment history.

Most credit reports have four categories:

- Identifying information

- Credit accounts

- Credit inquiries

- Public records

But every credit bureau is slightly different, so make sure to check what comes in your credit report before paying for one.

Credit bureaus are legally obligated to give you a free credit report once a year. There is no law requiring them to give you a free credit score.

Understanding Your Credit Score

A credit score provides more general information about your credit history.

Credit scores are based on credit reports and are placed on a scale of 300 to 850. They also typically come with a graphic indicating if your score is poor, fair, good, or excellent.

Your credit score is one of the biggest factors lenders use when considering loan applications; the higher the score, the more likely you are to pay your loan back.

If you don’t want to pay a credit bureau to get your credit score, you can use a free credit score site or take advantage of free services often provided by your credit card company. Keep in mind these scores might not be the most accurate, but they will give you an idea of where you fall on the scale.

Our article can help you better understand your personal credit score, including how exactly the score is calculated, what kind of things negatively impact your score, and why your credit score is important.

Did you know that your business has a credit score, too? Learn more about business credit scores and how you can check them.

Credit History VS Credit Score: The Bottom Line

At the end of the day, both your credit report and credit score are important to your business, potential lenders, and your financial health.

Credit scores are a great way to keep an eye on your overall credit health without needing to pay or read 4+ pages of detailed information. Credit reports are better for long-term planning, more detailed loan applications, and making important business decisions.

They both serve different purposes but inform each other. If you have questions about your report or score, contact the bureau that provided you with the information. There are dedicated support specialists ready and willing to help you understand what your report or score means.

Does your credit score need a bit of a boost? Check out a couple of easy ways for you to improve your personal credit score that you can start doing today!

Credit Report VS Credit Score FAQs

Kymberlin Bush

Expert Contributor

Kymberlin earned her Bachelor of Arts in Creative Writing from Pacific University in 2020 and resides in Portland, Oregon.

View Kymberlin Bush's professional experience on LinkedIn.

Latest posts by Kymberlin Bush (see all)

- TouchBistro VS Toast: Which Is Better For Your Restaurant? - March 13, 2024

- The Benefits Of A POS System - March 8, 2024

- The Benefits Of A Cloud-Based POS - March 8, 2024

- What Is A POS Transaction Fee? - March 8, 2024

- What Is The Main Purpose Of A Credit Bureau? - January 31, 2024