Do I Need Business Insurance? Coverage, Costs, & How To Choose

Read More

Apr 24, 2026

Filed under: Business Insurance

Loss run reports detail your business’s past insurance claims. Here's why you may need one.

WRITTEN & RESEARCHED BY

Editor & Senior Staff Writer

UPDATED

If you’re applying for business insurance, you may be asked for a loss run report.

Here’s what that means, why it matters, and how to get one.

Table of Contents

An insurance loss run is a report that details your business’s past insurance claims. Insurers use these reports to evaluate risk and help determine coverage and pricing.

A loss run report gives insurers insight into your claims history and overall risk. It can also help you compare quotes or negotiate premiums when shopping for coverage.

You can think of a loss run report as similar to a credit history for your business—it shows insurers how risky it may be to provide coverage.

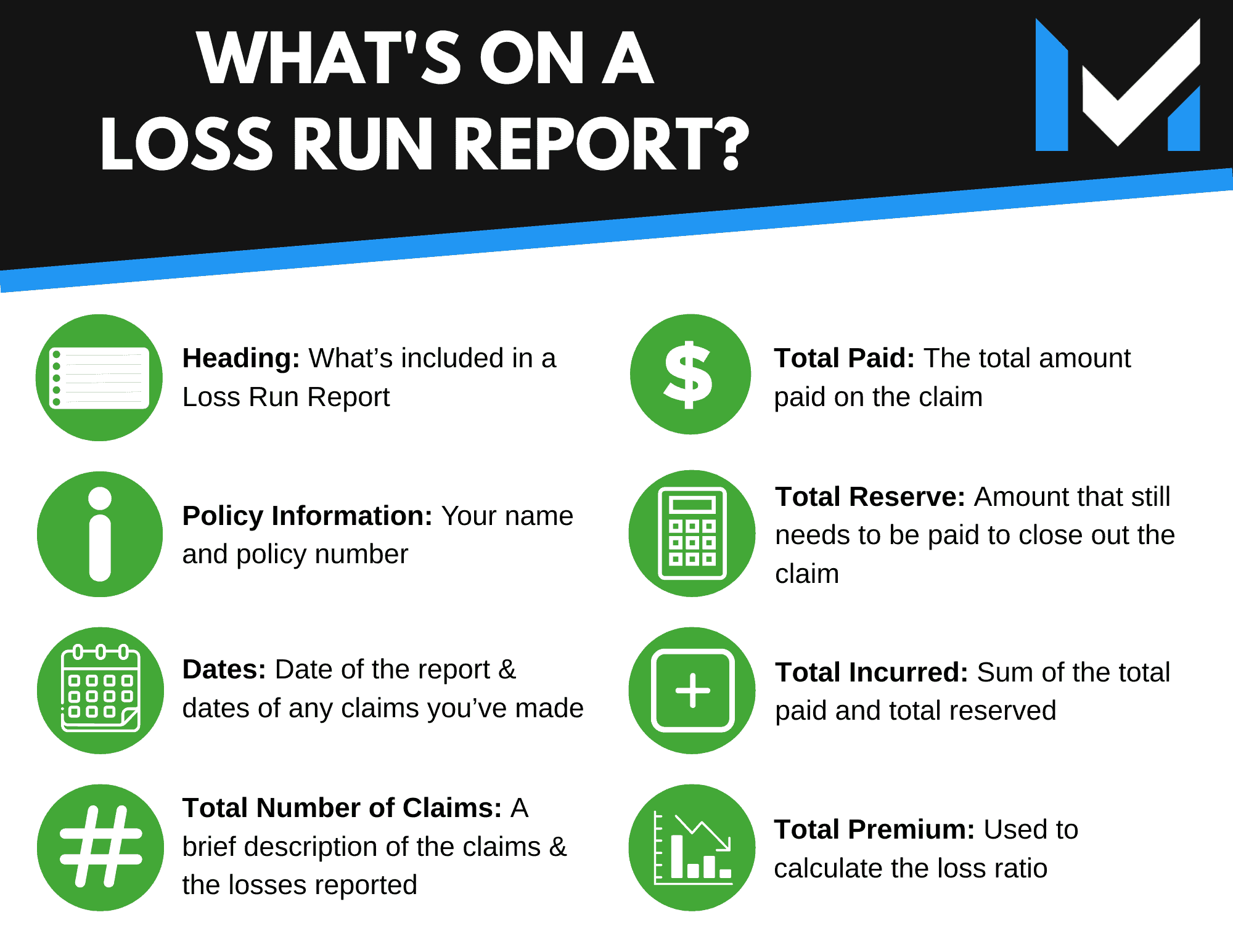

A loss run report typically includes:

There are a few common situations where you may need a loss run report:

Loss run reports are often required when applying for a new policy. Insurers use them to evaluate your claims history and assess risk before offering coverage or pricing.

If your business has few or no past claims, a loss run report can help you negotiate better rates. A strong claims history signals lower risk to insurers.

Loss run reports can help you identify patterns in claims, such as frequent incidents or higher-risk areas of your business. This information can be useful for improving safety practices and reducing future claims.

In many states, insurers are required to provide loss run reports within a set timeframe — usually within 10 business days after a request.

If you don’t receive your report within that period, you can follow up with your insurer or contact your state’s insurance department for guidance.

Getting a loss run report is usually a straightforward process. If you’ve worked with multiple insurers, you’ll need to request a report from each one.

Reach out to your insurance provider, broker, or agent by phone or email to request your loss run report.

Be prepared to share:

In many cases, insurers are required to respond within about 10 business days, though timing can vary by provider.

Loss run reports give you a clear view of your business’s claims history and overall risk.

They can help you identify problem areas, improve safety practices, and potentially secure better insurance rates. A strong claims history may work in your favor when comparing quotes, while a higher number of claims can lead to increased premiums.

Reviewing your loss runs regularly can help you spot patterns, reduce future risks, and make more informed decisions about your coverage.

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Experience competitive rates, excellent customer support, and a fast & easy claim process. Request a free analysis today.

Get Started

Experience competitive rates, excellent customer support, and a fast & easy claim process. Request a free analysis today.

Get Started

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.

Experience competitive rates, excellent customer support, and a fast & easy claim process. Request a free analysis today.

Get Started