Need help getting funds? Lendtek matches you with lenders instantly

Answer some basic questions in a few minutes with no impact to your credit score and compare multiple offers. No commitment, no hassle.

Get Matched💳 Save money on credit card processing with one of our top 5 picks for 2026

Understanding your credit report and how your credit score can impact small business loans is a crucial aspect of your small business.

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

REVIEWED BY

Expert Contributor

Whether you need to know for a small business loan application, personal use, or general management of your business, it’s important to understand how credit reports and credit scores differ.

Table of Contents

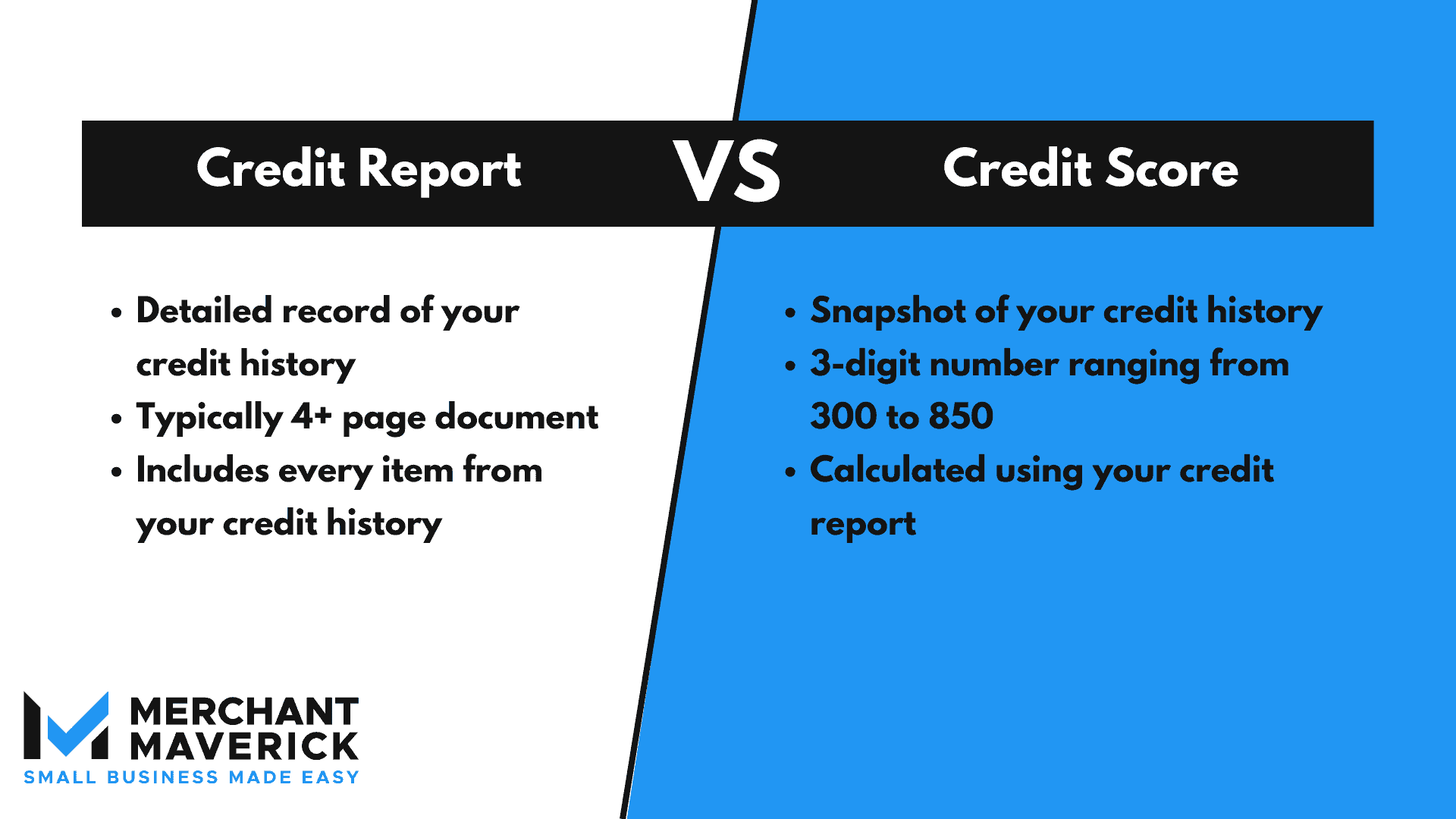

Your credit report is going to provide detailed information about your credit history, while your credit score provides a much more general snapshot of your current credit standing. You can use any credit bureau to receive a credit report, but the main three are Experian, TransUnion, and Equifax.

Some lenders will refer to a credit report more generally as your credit history. So, if you are asked to provide your credit history versus your credit score, you’ll want to use a credit bureau to obtain an up-to-date credit report.

On a credit report, you’ll see detailed information about your credit history.

A typical credit report will give you a full breakdown of all your open or closed credit accounts, bank accounts, loans, and payment history.

Most credit reports have four categories:

But every credit bureau is slightly different, so make sure to check what comes in your credit report before paying for one.

Credit bureaus are legally obligated to give you a free credit report once a year. There is no law requiring them to give you a free credit score.

A credit score provides more general information about your credit history.

Credit scores are based on credit reports and are placed on a scale of 300 to 850. They also typically come with a graphic indicating if your score is poor, fair, good, or excellent.

Your credit score is one of the biggest factors lenders use when considering loan applications; the higher the score, the more likely you are to pay your loan back.

If you don’t want to pay a credit bureau to get your credit score, you can use a free credit score site or take advantage of free services often provided by your credit card company. Keep in mind these scores might not be the most accurate, but they will give you an idea of where you fall on the scale.

Our article can help you better understand your personal credit score, including how exactly the score is calculated, what kind of things negatively impact your score, and why your credit score is important.

Did you know that your business has a credit score, too? Learn more about business credit scores and how you can check them.

At the end of the day, both your credit report and credit score are important to your business, potential lenders, and your financial health.

Credit scores are a great way to keep an eye on your overall credit health without needing to pay or read 4+ pages of detailed information. Credit reports are better for long-term planning, more detailed loan applications, and making important business decisions.

They both serve different purposes but inform each other. If you have questions about your report or score, contact the bureau that provided you with the information. There are dedicated support specialists ready and willing to help you understand what your report or score means.

Does your credit score need a bit of a boost? Check out a couple of easy ways for you to improve your personal credit score that you can start doing today!

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Our expert reviewers found BusinessLoans.com to have a quick and easy application process alongside excellent support and guidance for borrowers.

Start A Quick Application

Our expert reviewers found BusinessLoans.com to have a quick and easy application process alongside excellent support and guidance for borrowers.

Start A Quick Application

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.

Our expert reviewers found BusinessLoans.com to have a quick and easy application process alongside excellent support and guidance for borrowers.

Start A Quick Application