Home Equity Loans VS HELOCs: Can You Use Home Equity Loans & HELOCs For Business?

Home equity loans and HELOCs offer low interest rates, long repayment periods, and are easier to qualify for than other business funding options, but should you use this risky method?

-

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

-

REVIEWED BY

Editor & Senior Staff Writer

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

Key Takeaways

- Home equity loans and HELOCs offer lower interest rates than most business funding, but your home is on the line if you can’t repay.

- Home equity loans give you a lump sum with fixed payments, while HELOCs offer flexible access to funds with variable rates.

- They’re easier to qualify for, but established businesses may find safer funding options without risking personal assets.

Home equity loans and home equity lines of credit (or HELOCs) allow individuals to borrow against their home equity. While these types of lending are generally used for home improvements, they can be used for business expenses, as well.

But how exactly do home equity loans and HELOCs work, and are they a good choice for funding your business?

They can be a strong funding option for some businesses — especially startups — but they come with serious risk since your home is on the line.

Let’s dive into the long answer to see if you’re one of the businesses that could benefit from a home equity loan for business or a HELOC for business.

Table of Contents

- What Is A Home Equity Loan?

- What Is A HELOC?

- Home Equity Loan VS HELOC

- Home Equity Loans & HELOCs Closing Costs & Fees

- When To Use A Home Equity Loan For Business

- When To Use A HELOC For Business

- When To Use A Lending Alternative To Home Equity Loans & HELOCs

- Where To Find A Home Equity Loan Or HELOC For Your Business

- The Bottom Line On Using Home Equity Loans & HELOCs For Business

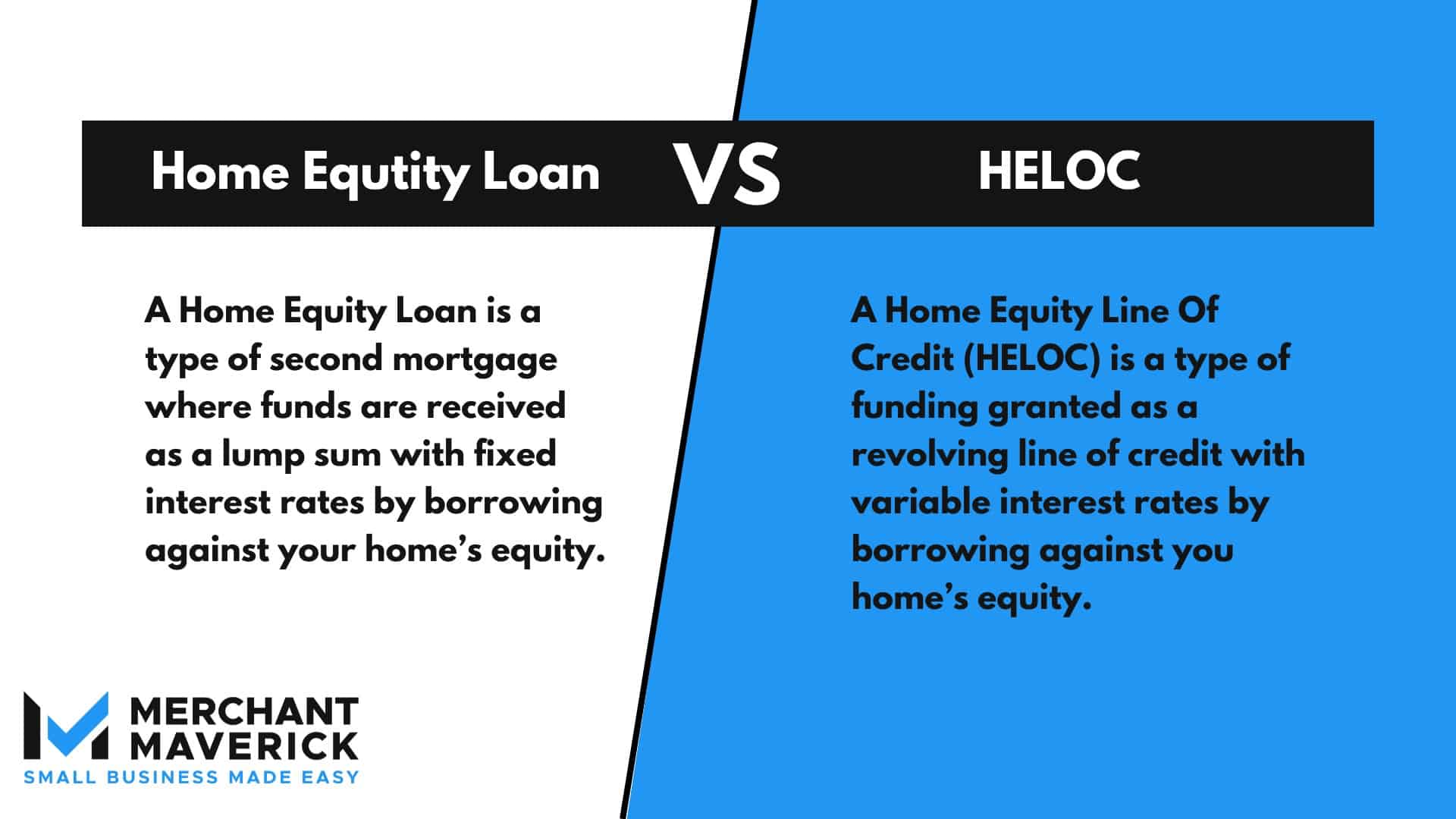

What Is A Home Equity Loan?

A home equity loan is a type of second mortgage where you can take out a loan against the equity on your home.

While home equity loans are primarily used for home improvements and renovations, they can also be used to consolidate debt, pay off credit cards, finance student loans, and even start or fund a small business.

Some advantages of using home equity loans for business are that home equity loans generally have lower interest rates and are easier to qualify for than other types of small business lending. They also are more flexible than other small business loan options because they can be used on a wide variety of business expenses.

However, taking out a loan against the equity of your home is no easy decision and comes with significant risk. With home equity loans, the collateral on that loan is your home, so if you default on the loan, you risk foreclosure. If your home’s property value decreases with fluctuation in the real estate market, you also risk going upside down on your loan (i.e. owing more than your home is worth).

Pros and cons to consider when it comes to home equity loans for business include:

Pros

-

Low interest rates

- Fixed interest rates

-

Long repayment periods

- Good for startups with no business credit or business history

-

Easier to qualify for than other business funding options

- Potentially larger borrowing limits than other business funding options

-

Can be used for a wide variety of business expenses

- Potential interest tax deductions

Cons

-

Have to use your home as collateral

-

Defaults on your loan could lead to foreclosure

-

You still have to pay back the loan if your business fails

-

Could go upside down on your loan if home value drops

-

Closing costs & several other upfront fees required

-

Potentially more interest paid overall than a HELOC

How Does A Home Equity Loan For Business Work?

True to its name, a home equity loan depends entirely on your home’s equity.

Home equity is the amount of value you have in your home. Home equity is the difference between how much you owe on your home and the value of the property.

However, not every small business is going to be able to get a home equity loan or a HELOC, as the equity of your home generally has to be at least 20% of your home’s market value to be approved by lenders.

So, how do you know how much home equity you have and if you can qualify for a home equity loan?

Here’s how to calculate your home equity:

Current Home Value – Current Mortgage = Home Equity

So, if you have a $300,000 house and owe $200,000 left, you’d have $100,000 in home equity. To turn this into a percentage, divide your home equity amount by your current home value and multiply by 100. So, in this case, 100,000/300,000=.33 x 100 = 33 or 33%.

To get a home equity loan, you’ll need at least 20% home equity to qualify. Most lenders allow you to borrow up to 80% to 85% of your home’s total value, minus what you still owe on your mortgage. So in a $300,000 home with $200,000 owed, you could potentially borrow up to $40,000 – $55,000 (80% – 85% of $300,000 minus $200,000).

With enough equity, a person can take out a loan against their home equity by offering up their house as collateral for the loan. You will likely have to have a home appraisal and title search done to verify your home value and apply for this type of loan. Because home equity loans operate as a type of second mortgage, you will have to pay closing cost fees (among other fees).

As a second mortgage, a home equity loan is subordinate to your primary mortgage — meaning in the event of foreclosure, your primary mortgage lender gets paid first. This subordinate position makes home equity loans slightly riskier for lenders, which is why credit and equity requirements apply.

Your lender may also require title insurance. Make sure your lender discloses all fees, and be sure to factor these costs into your decision on taking out a home equity loan. If these fees are too much, a HELOC might be a better way to use your home equity.

Once you have been approved for your home equity loan, gone through underwriting, and paid the appropriate fees, you will be given a lump sum to use on just about anything you wish. You can expect a repayment period of 5 to 30 years with fixed interest rates which leads to more predictable monthly payments.

As with all loans, make sure to check if your lender has any pre-payment penalties.

Home Equity Loan Requirements

Because you have to offer your home as collateral, home equity loans, while risky for individuals, are fairly secure for banks, which means banks can offer home equity loans with far fewer requirements than other loan options.

To qualify for a home equity loan, you have to:

- Have at least 20% home equity

- Agree to offer your home as collateral

- Have a debt-to-income ratio of 43% or lower

- Have a consistent revenue source (generally 2 years of stable income)

While there usually isn’t a specific credit score required for a home equity loan, the better your credit, the lower your interest rates will be. Home equity loans are most competitive for individuals with good to excellent credit, as individuals with poorer credit are less likely to get the low interest rates that make a home equity loan worthwhile.

Because approval is based on your personal finances — not your business –home equity loans can be easier for startups to qualify for.

What Is A HELOC?

HELOC stands for home equity line of credit. Like a home equity loan, HELOCs are based on an individual’s home equity, but instead of a lump sum, HELOCs offer a revolving line of credit.

Much like a home equity loan, you can use a HELOC for a variety of expenses, including home improvements, debt consolidation, student loans, emergency funds, and — you guessed it — small business expenses.

With a HELOC, you still have to offer your home as collateral, but you only have to repay the money you actually spend on your credit line (much like how a credit card gives you access to a credit balance, but you only have to repay what you spend).

Here are some additional pros and cons of HELOCs:

Pros

-

Revolving line of credit

-

Fewer fees than a home equity loan

-

Long repayment periods

-

Easier to qualify for than other business funding options

-

Good for startups with no business credit or business history

-

Can be used for a wide variety of business expenses

-

Potentially less interest than a home equity loan

Cons

-

Variable interest rates

-

Variable monthly payments

-

Have to use your home as collateral

-

Defaulting on your loan could lead to foreclosure

-

New line of credit could affect your credit score

How Does A HELOC for Business Work?

A HELOC is like a line of credit or credit card in that it grants you access to a credit limit that you can use as needed by using your home equity to determine your borrowing amount and offering your home as collateral. A key distinction between a HELOC and a traditional line of credit or credit card is that HELOCs have two distinct phases — the draw phase and the repayment phase.

The drawing phase, or draw period of a HELOC loan, is the time frame during which you can spend your HELOC borrowing limit as needed. Whether it’s equipment purchasing, onboarding, marketing, you name it, the draw period is the time to make those purchases.

During the draw period, you’ll have to make minimum payments like with a credit card. The draw period usually lasts 10 years.

After the draw period, you’ll no longer be able to use the HELOC for new purchases and will instead enter the repayment phase, or repayment period, where you’ll be expected to make monthly payments on the principal and interest you owe. Remember, HELOCs have variable interest rates, so monthly payments are not fixed. Make sure you have ample wiggle room to cover your HELOC payment, or you risk losing your house.

Most HELOCs include a lifetime rate cap — a maximum interest rate the lender can charge. This provides some protection against extreme rate increases. Ask your lender about their specific rate cap before signing.

We recommend going with a HELOC without a prepayment penalty and paying more than your minimum payment throughout the draw phase to lower the overall interest you owe. The repayment period usually last 10-20 years.

Like a home equity loan, a HELOC will be based on your home equity, and 20% home equity is needed to qualify.

HELOC Requirements

HELOC requirements are very similar to home equity loans:

- Have at least 20% home equity

- Agree to offer your home as collateral

- Have a low debt-to-income ratio (at least 43% or less)

- Have a consistent revenue source (generally 2 years of stable income)

Having a good to excellent credit score is also recommended, as you will be able to get a more favorable interest rate.

The requirements for HELOCs could make it easier for startups with no business history, business credit score, or revenue to get access to funds.

However, putting up your home as collateral is no light decision.

No one wants to think that their business will fail, but this is a potential reality you have to consider before agreeing to a home equity loan or HELOC because even if your business fails, you are still responsible for repaying your home equity loan or HELOC (unlike other business funding options where you borrow against your business rather than yourself as an individual).

This is especially important to consider because the repayment periods for both HELOCs and home equity loans are much longer than traditional business lending options.

Home Equity Loan VS HELOC

| Home Equity Loan | VS | HELOC |

|---|---|---|

| Fixed interest rate | Variable interest rate | |

| Lump sum | Revolving line of credit | |

| Predictable monthly payments | Variable monthly payments | |

| Higher interest rates | Lower interest rates |

While both home equity loans and HELOCs rely on your home equity for funding and use your house as collateral, they work quite differently. The key difference: home equity loans give you a lump sum, while HELOCs give you flexible access to funds.”

Another difference is that most HELOCs come with variable interest rates, whereas most home equity loans have fixed rates. While the fixed rates of a home equity loan provide stability and a more predictable monthly payment, you’ll often find that home equity loans have a higher interest rate than HELOCs.

So which is better: a home equity loan or a HELOC?

Whether a home equity loan or a HELOC is right for your business is going to depend significantly on what you plan on using the funds for.

If you have a larger business purchase to make, such as buying equipment or purchasing real estate, the lump sum offered through a home equity loan is the wiser choice.

If you want a more flexible funding option for working capital, hiring new employees, purchasing inventory, or having a backup emergency funds option, a HELOC may be the better option for your business. A HELOC is also often a better option if you aren’t 100% sure how much your purchase is going to be, as you only pay back what you use, whereas if you get a $50,000 home equity loan and only end up using $20,000 of it for your business expenses, you still have to pay back the full borrowing amount of $50,000.

Home Equity Loans & HELOCs Closing Costs & Fees

Like a mortgage, both home equity loans and home equity lines of credit are subject to closing cost fees.

Closing cost fees generally range between 2%-6% of your borrowing amount or credit limit.

Beyond closing costs, you may also encounter:

| Home Equity Loan Fee | Amount |

|---|---|

| Closing Costs | 2%-6% |

| Origination Fee | 0.5%-1% |

| Home Appraisal Cost | $300-$800 |

| Title Search Fee | $75-$200 |

| Credit Report Fee | $10-$100 |

| Application Fee | Varies |

| Underwriting Fee | Varies |

Some lenders may charge an inactivity fee, minimum withdrawal fee, and/or a transaction fee for HELOCs.

Both HELOCs and home equity loans can be subject to prepayment penalties, so be sure that your lender discloses all fees and shop around for a lender that doesn’t charge fees you aren’t comfortable with. You may even find a lender that will cut down or waive the closing cost fees entirely.

When To Use A Home Equity Loan For Business

A home equity loan may be a good fit if you want a low, fixed-rate loan with predictable monthly payments.

You’ll receive a low fixed rate and a longer period of time to repay your loan. You may even qualify for additional savings if you work with the lender of your first mortgage.

Here are the situations where a home equity line of credit could be a good fit for your business:

- If you are a startup with no business credit, history, or revenue

- If you have strong personal credit and can get a much lower interest rate with your home equity loan vendor than a traditional business loan

-

If you don’t qualify for a low-interest SBA loan instead

- If you want a longer repayment period with a predictable fixed interest rate

-

If you need more flexible spending to fund business expenses not covered by traditional business loans or SBA loans

- If you would qualify for tax deductions on your home equity loan’s interest payments

While home equity loans can have their place for business funding, there are also times when a home equity loan isn’t the best fit.

If you have an established business and a solid personal credit profile, you could qualify for other types of funding, such as Small Business Administration loans. These loans come with low interest rates, repayment terms up to 25 years, and are easier to qualify for than traditional bank loans.

You might also want to explore additional funding options if you need more specialized financing. For example, if your business needs new equipment, equipment financing may be a better option. You could potentially qualify for low rates and favorable terms without putting your personal assets on the line. With equipment leases, you can even turn in your equipment and enter another lease for new equipment, which can be a great move if you need to upgrade frequently.

Plus, all of these alternatives keep you from having to offer up your home as collateral.

When To Use A HELOC For Business

A HELOC is a better fit if you want flexible access to funds and only pay interest on what you use. HELOCs are also a good fit if you want lower interest rates and longer repayment periods than other business loans.

A HELOC could be a good choice for your business if:

-

If you are a startup with no business credit, history, or revenue

- If you have strong personal credit and can get a much lower interest rate with your HELOC vendor than a traditional business line of credit or credit card

-

If you want a longer repayment period

- If you need more flexible spending to fund business expenses not covered by traditional lines of credit

-

If you would qualify for tax deductions on your HELOC’s interest payments

The final question you’ll need to answer before choosing a HELOC. For businesses considering a HELOC, make sure the pros outweigh the cons and that you’ve looked into all business funding alternatives before committing to a home equity line of credit.

When To Use A Lending Alternative To Home Equity Loans & HELOCs

The same reasons home equity loans and HELOCs are appealing for startup and business funding are why they are so risky. Home equity loans and HELOCs are relatively easy to qualify for and have no business requirements (like time in business, business income, etc.) because you have to use your home as collateral instead.

While both home equity loans and HELOCs generally have much smaller interest rates than other small business funding options, taking out a loan or line of credit against your home is no small thing.

Don’t use a home equity loan or HELOC if:

-

You Aren’t Comfortable Using Your Home As Collateral: Taking a loan or line of credit out against your home, which is often most people’s biggest asset, is no light decision. The risk of foreclosure could be too great, especially for startups who are unsure if their business endeavors will actually pay off.

- You Don’t Have A Stable Income Stream For Making Monthly Payments: Remember that you as an individual are responsible for repayments no matter how your business does and that a default equals foreclosure, so make sure you can cover monthly payments without banking on business income for those payments.

-

You Don’t Have Over 20% Equity In Your Home: You need a minimum of 20% home equity to qualify for this type of funding. Look into other small business funding options or improve your home equity first by increasing your home’s value and paying down your mortgage.

- You Can’t Afford The Closing Costs: Both home equity loans and home equity lines of credit have some hefty fees associated, like closing costs, that you’ll need to factor into your budget if you go with the home equity financing route.

-

You’re Worried That Your Home Value Will Significantly Drop: If you’re not careful, you could be looking at negative equity (i.e. owing more than your home is worth), so taking out a home equity loan or HELOC during a volatile real estate market could be problematic.

- You’re Planning On Moving Soon: In most cases, you can still move if you have a HELOC or a home equity loan, but it does make the process more complicated. If you are planning on moving, you will have to pay off the home equity loan or HELOC (and any prepayment penalties) with the proceeds from the sale, so make sure you have enough money to cover this. And if you are likely to move soon, maybe delay your home equity funding search or look into other business loan options.

Luckily, there are many great alternatives to home equity loans and HELOCs available for business owners.

Like home equity loans, small business loans, while potentially more difficult to qualify for, offer you a lump sum for certain business expenses and don’t risk your home. SBA loans can be a bit easier to qualify for than private lenders because they are government-backed, so looking into and understanding SBA loans can definitely be worth it.

Business credit cards and business lines of credit can both operate similarly to HELOCs in that you’ll have access to a credit limit to spend on business expenses as needed. And there are always business grants as well, which can be particularly helpful for certain startups.

For startups without a business history, finding viable business funding options can be trickier.

Where To Find A Home Equity Loan Or HELOC For Your Business

If you’ve decided a home equity loan or home equity line of credit is right for your business, start by seeing if your existing mortgage lender or bank offers home equity loans and HELOCs. You may be able to get a good deal working with a lender that already knows your track record.

Once you get an offer from your lender or banking institution, make sure to shop around with other popular home equity loan or HELOC providers so that you get the best terms and rates possible.

Note that most lenders should only do soft credit pulls that do not affect your credit score during the initial stages, but be sure to check that you won’t be hit with an unexpected hard credit pull that could affect your credit score negatively.

How To Get A Home Equity Loan For Business

If you meet the qualifications for a home equity loan, follow this seven-step process to get a home equity loan for your business:

- Step 1: Get Your Home Appraised

- Step 2: Calculate Your Home Equity

- Step 3: Search For A Home Equity Loan Lender

- Step 4: Fill Out Your Application

- Step 5: Pay Your Closing Costs & Other Fees

- Step 6: Get Your Business Funds In A Lump Sum

- Step 7: Make Regular Monthly Payments

How To Get A HELOC For Business

If you meet the requirement for a home equity line of credit, you can follow these eight steps to get a HELOC for your business:

- Step 1: Get Your Home Appraised

- Step 2: Calculate Your Home Equity

- Step 3: Search For A Home Equity Loan Lender

- Step 4: Fill Out Your Application

- Step 5: Pay Your Closing Costs & Other Fees

- Step 6: Get Your Business Funds In A Revolving Line Of Credit

- Step 7: Spend As Needed During The Draw Period & Make Minimum Payments

- Step 8: Enter The Repayment Period & Pay Back Principal Plus Interest

The Bottom Line On Using Home Equity Loans & HELOCs For Business

A home equity loan certainly has its benefits — startups can qualify, interest rates are low, and terms are favorable. However, there may be other options that make sense for your business that don’t put the roof over your head at risk. As with any other loan, shop around, compare lenders, and understand the terms of your loan or line of credit before signing a contract.

Still undecided if a home equity loan is right for you? This risky funding certainly isn’t for everyone, and you may find that another financial product offers better peace of mind while still fitting your business’s capital needs. Before taking the leap into a home equity loan or home equity line of credit, consider these top small business loans or these best small business credit cards as alternatives.

Chelsea Krause

Expert Contributor

Chelsea Krause is a writer who specializes in accounting, payroll, and small business loans. She has been helping small business owners manage their finances since 2016. She is a QuickBooks Certified User and former eCommerce store owner. Her accounting expertise has been quoted in Forbes and her work appears in Startup Nation, Small Business Bonfire, and Women on Business. Chelsea graduated summa cum laude with a BA in English & Creative Writing from George Fox University and studied abroad at the University of Oxford as well.

View Chelsea Krause's professional experience on LinkedIn.

Latest posts by Chelsea Krause (see all)

- TimeTrex Workforce Management Review - October 15, 2024

- eSmart Paycheck Review - October 15, 2024

- U.S. Bank Commercial Rewards Card Review - September 26, 2024

- U.S. Bank Business Banking Review - September 26, 2024

- Prime Alliance Bank Review - September 25, 2024