Merchant Category Codes (MCC): What They Are & How To Find Yours

Merchant category codes are assigned to your small business by your credit card processing company. Find out more about them in this complete guide to MCCs.

-

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

-

REVIEWED BY

Expert Contributor

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

Key Takeaways

- MCCs are four-digit codes assigned to businesses by credit card networks to categorize the type of goods or services they offer, impacting interchange fees and rewards eligibility.

- Certain MCCs affect how transactions are reported to the IRS, particularly for industries like travel and entertainment.

- Choosing the correct MCC is crucial for avoiding higher processing fees and ensuring proper transaction handling.

MCC codes or merchant category codes probably aren’t something you’re thinking about when you sign up for your first merchant account.

However, understanding how MCC codes fit into the larger landscape of payment processing can help you make better strategic decisions and, at the very least, give you a better sense of why your business is treated the way it is by banks, credit card networks, and processors. When hunting for the best merchant accounts, you’ll want to be armed with the best knowledge, so you can get the best rate.

Read on, and we’ll demystify merchant category codes for you.

Table of Contents

What Are MCC Codes?

A merchant category code, or MCC, is a four-digit number that indicates your line of business and the types of goods or services you provide to your customers. MCCs are assigned to merchants by credit card companies. These codes can affect the interchange fees (or tiered fees) you are charged for credit card transactions.

How Are MCC Codes Used?

Originally developed to simplify accounting for the year-end 1099 tax form reporting, the MCC code is now a critical piece in the payments landscape. While the International Organization for Standardization (ISO) sets the MCC codes and meanings, credit card issuers nowadays assign the codes to merchants.

These credit card merchant codes are then used by acquiring banks and payment service providers to set fees, assess risk, and more. Keep in mind that each card network—Visa, Mastercard, Discover, and American Express—has its own list of MCCs. While they are largely similar, there might be some specific differences for certain types of businesses.

What Are The MCC Code Categories?

Specific merchant category codes vary by card network. For example, Visa and Mastercard may assign slightly different codes to the same merchant.

The broad MCC categories are:

- Agricultural services

- Contracted services

- Transportation services

- Utility services

- Retail outlet services

- Clothing stores

- Miscellaneous stores

- Business services

- Professional services and membership organizations

- Government services

How Do MCC Codes Affect Payment Processing?

Since your MCC code represents the “predominant business activity of the merchant,” it can influence payment processing in a few different ways.

Can Getting The Right MCC Really Lower Your Processing Costs?

In some cases, it may be possible to lower your credit card processing costs by changing your classification.

Visa and Mastercard both offer lower interchange rates to “emerging markets” — that is, businesses that historically haven’t accepted credit cards as their predominant form of payment. That includes healthcare and education as well as government organizations, utilities, and even insurance sales. Of course, specific requirements apply to be qualified for these MCC codes.

Can You Change Your MCC Code?

Merchants can request a review of their current merchant category code, but how you’re classified is ultimately it’s up to your card issuer.

For more information on special interchange rates that businesses can qualify for with the right MCC code, check out our complete guide to B2B credit card processing.

How To Do A MCC Code Lookup

Doing a merchant category code lookup isn’t always convenient. You may or may not find it on your merchant statement, and if you don’t know how to find your merchant category code or do a little digging, you may not even know what it is at all!

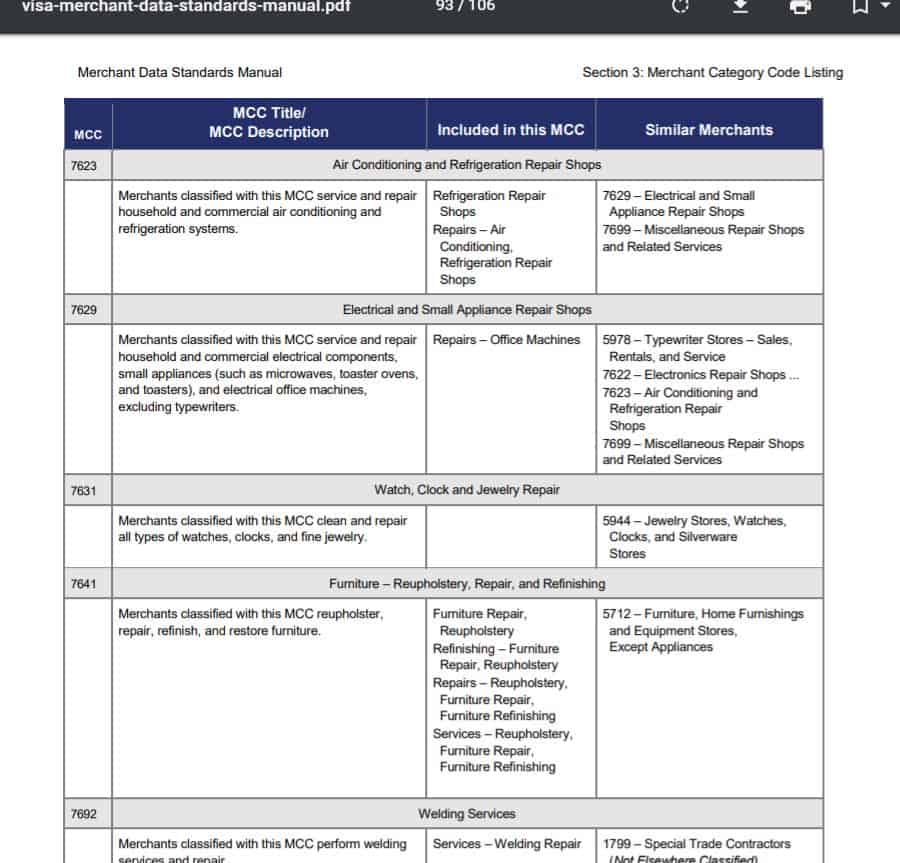

A great source of information about merchant categories and related policies and guidelines is the Visa Merchant Data Standards Manual. Here you can see that even under a general blanket (e.g., repair shops), the codes get a lot more specific depending on the products and services a merchant provides. Keep in mind that your card issuer may use a different set of criteria, so it’s never a bad idea to ask your payment processor directly.

When Should You Update Your MCC Code?

Most businesses probably won’t run into serious issues with their MCC Codes, but there are times when it’s worth looking into updating your code with your payment services company. Instances in which you may want to push the issue include:

- Your Business Has Changed: Maybe you’ve started selling different products, offering new services, or changing the way you’re marketing your business. It’s possible your MCC code no longer accurately reflects how your business operates.

- You’re Getting An Unusual Number Of Declined Transactions: If you’re seeing a conspicuous increase in declined transactions that your customers can’t explain, it may be time to see if your MCC code is accurate.

The Final Word On MCC Codes

MCC codes are a critical component of every business when it comes to accepting credit cards. They are decided by credit card processors at the start of the application process and indicate what type of business you have and what products or services you provide.

Understanding how this code affects you can help you decide whether or not to register as a nonprofit or request that additional MCC codes apply to an expanding part of your business. Beyond reaching out to your credit card processor, however, there isn’t much you can do as a business owner to make the final decision about your MCC code, as it’s based on specific criteria identified by the credit card processor at the time of your application.

Need more information on credit card processing? We have a world of resources waiting for you. Start by checking out our article on small business credit card processing companies not only to see some top picks but also to learn what to look for when you’re shopping around.

Chris Motola

Expert Contributor at Merchant Maverick

Chris has been writing about small business topics since 2003. He has been featured in Fox Business, ABC News, Yahoo Finance, GoBankingRates, Newsweek, BizJournals, and other publications. He has a Bachelor’s of Arts in English Writing Arts from SUNY Oswego, and a Masters of Science in Interactive Media from the University of Central Florida.

View Chris Motola's professional experience on LinkedIn.

Latest posts by Chris Motola (see all)

- Credit Card Company Market Share - March 19, 2024

- Largest Credit Card Networks - March 19, 2024

- The Biggest Credit Card Issuers - March 19, 2024

- Largest Payment Processors - January 17, 2024

- The Complete Guide To ACH Processing Fees - November 30, 2023