Mobile Credit Card Processing Reviews

-

Square

Read Review Visit SiteSquare Payments earns a perfect 5-star rating for ease of use, astounding feature set, transparent and affordable pricing, and overall status as a powerhouse for merchants. While Square's payment processing service is not appropriate for all business types and lacks the stability and negotiability of a standard merchant account, many small businesses enjoy the predictable pricing and the lightning-quick setup.

-

Clover Go

Read Review Visit SiteClover Go looks like any other mobile processing app out there. Unfortunately, small businesses are going to encounter inconsistent pricing and potentially awful customer support. Check out our Clover Go review to see if it's really the best option for you!

-

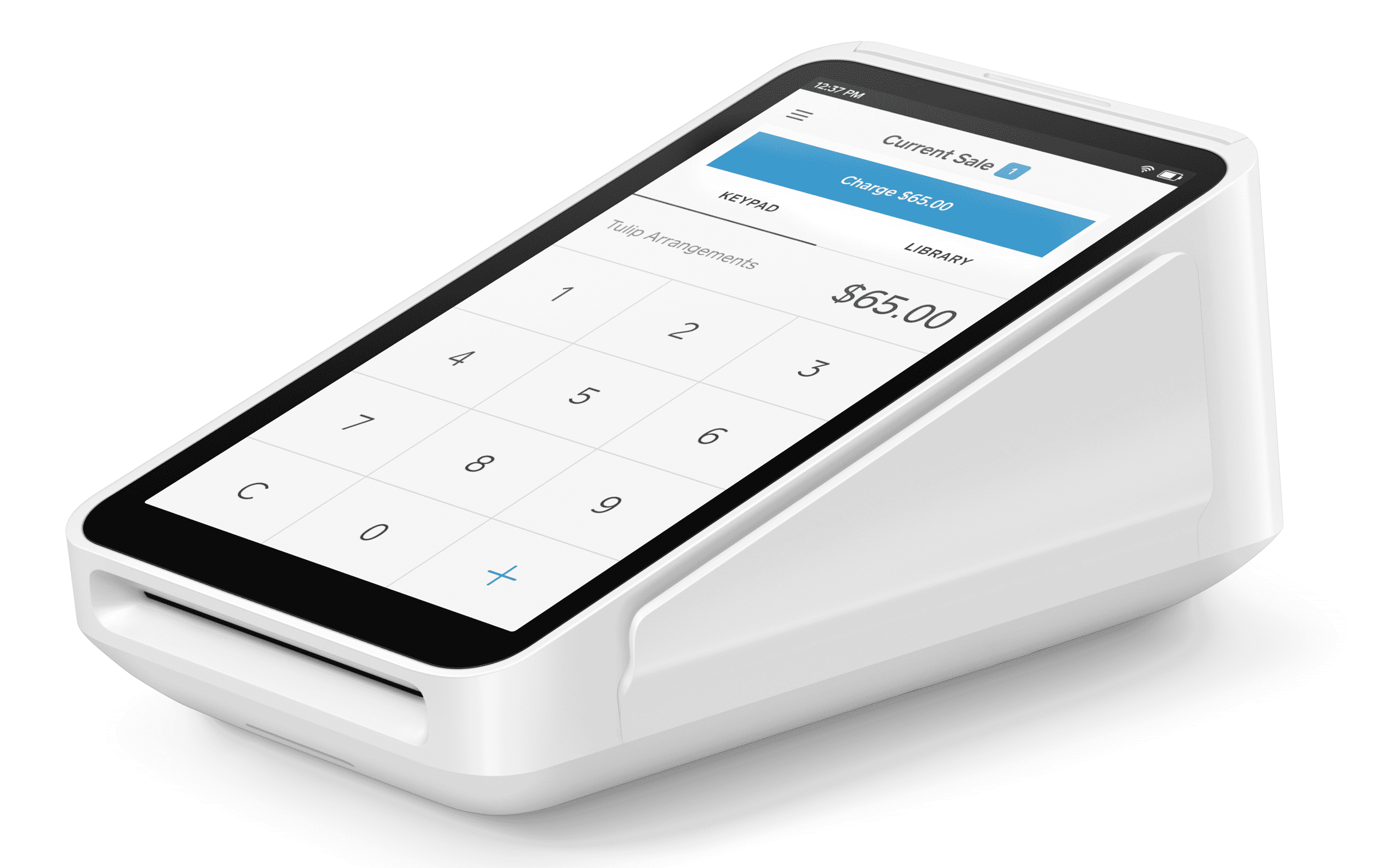

Square Terminal

Read Review Visit SiteSquare Terminal combines Square’s mobile POS app with an integrated card reader, all in a compact handheld device. Check out our in-depth review to see if it’s really worth the investment.

-

SumUp

Read Review Visit SiteSumUp’s free mobile processing app isn’t a good substitute for a full POS system, but for small businesses that only need basic POS features and on-the-go credit card processing, it’s definitely a contender.

-

QuickBooks GoPayment

Read Review Visit SiteQuickBooks GoPayment (formerly Intuit GoPayment) enables taking payments on the go, and for most merchants, the draw of GoPayment is probably that it syncs with QuickBooks Online. The seamless QuickBooks integration makes it easy for you to keep track of your funds and expenses on the go.

-

PayPal Point of Sale

Read Review Visit SitePayPal offers a comprehensive suite of services for merchants, from the mobile POS app (the focus of this review) as well as online card processing, business financing, POS partnerships, and much more. Want to use PayPal POS to get paid? PayPal Here is becoming PayPal Zettle — read our updated review for more about features and pricing.

-

Zettle by PayPal

Read Review Visit SiteWith no monthly minimum fees, no binding contracts or cancellation fees, and a growing number of feature options, it's clear that iZettle is worth a generous amount of consideration for mobile processing. While iZettle now serves a dozen countries, including Italy, Mexico, Brazil, Sweden, and Germany, we focus on the company's UK services for this review.