Best Credit Card Processing Companies In 2024

Read More

May 29, 2024

Filed under: Credit Card Processing

Despite offering businesses excellent rates, Citibank Business Loans have stringent borrower qualification and opaque terms that make it challenging for prospective borrowers.

WRITTEN & RESEARCHED BY

Lead Staff Writer

Last updated onUpdated

REVIEWED BY

Lead Staff Writer

| Total Rating | 2.7 |

|---|---|

| Rates & Fees2.9 | |

| Services5.0 | |

| Eligibility Requirements1.7 | |

| Application1.0 | |

| Sales & Advertising Transparency2.2 | |

| Customer Service2.8 | |

| User Reviews2.1 | |

Table of Contents

Citibank is a popular bank that provides personal and business financing. Citibank offers several lending products to small businesses, including term loans and lines of credit. Loans from Citi are considered among the most competitive in the business, but they can be difficult to qualify for. This is compounded by the bank’s opaque borrower requirements, which make it difficult for businesses to know if they would qualify in the first place.

| Services5.0 |

|---|

| Lending Services 5.0 |

| Lending Limits 5.0 |

| Payment Portal & Mobile App 5.0 |

Citibank offers a solid selection of business lending options that meet a variety of lending needs, putting the lenders rating in this section at 5/5.

Citibank provides the following lending products to qualified businesses:

Since our last review, Citibank has also added SBA loans and lines of credit to the mix.

Though bank loans such as Citibank business loans are generally suited to larger, established businesses, Citi offers loans to small businesses as well. In particular, smaller businesses will be interested in Citibank’s installment loans for purchasing fixed assets — such as equipment or lines of credit for short-term or recurring cash flow needs. Those lending products are available in amounts as small as $5,000 and $10,000, respectively.

While it’s not a loan, Citibank also offers small business credit cards, which may be more appropriate for small businesses that don’t qualify for a loan.

| Eligibility Requirements1.7 |

|---|

| Availability 3.0 |

| Borrower Qualifications 1.3 |

| Transparency 1.0 |

Citibank plays its cards pretty close to its chest, but most qualifying companies will need to have been in business for at least two years. Citibank doesn’t disclose credit requirements, but you can expect to have a hard time qualifying if your credit score is below the 600 mark. Similarly, there are no explicit income requirements, but it’s good business practice to have $1.25 worth of revenue for every $1 of debt you’re servicing.

| Time in business: | 2 years |

| Credit score: | Unknown |

| Revenue: | Unknown |

Additionally, Citibank may impose geographic restrictions on some of its business lending products, and you will also need to have a Citibank business banking account, as well as personal guarantees from all owners collectively owning 51% or more of the business. Citibank gets a 1.7/5 star rating for this section for the lack of transparency and the fact that some Citibank loans are limited by location and to businesses with a Citibank bank account.

| Rates & Fees2.9 |

|---|

| Pricing 5.0 |

| Affordability 0.8 |

Citibank offers installment loans and lines of credit to businesses in both secured and unsecured forms. Citibank also provides healthcare acquisition financing and commercial mortgages. Generally, bank loans including Citibank offer lower interest rates than what you would expect from an online loan.

Unfortunately, the bank is extremely opaque when it comes to terms and fees, divulging almost none of that information publicly, resulting in a section rating of 2.9/5 stars.

To get information on interest rates, origination fees, and other fees, you’ll need to speak with a specialist by requesting a call or visiting your local Citibank branch.

If you qualify for the Citibusiness Preferred Program, you may be eligible for waived origination fees, discounted interest rates, and other benefits.

Citibank is at least open about borrowing amounts, term lengths, and interest rate types:

Citibank also has a larger line of credit for businesses that need from $250,000 to $5,000,000.

| Application1.0 |

|---|

| Application Process 1.0 |

| Application Timeline 1.0 |

Keeping up with the theme of non-transparency, Citibank does not disclose much information about its application process, approval timeline, or time to funds once your application is approved.

Expect to have to provide information about your business, your bank accounts, and your resources. If you have business partners, you’ll likely need their information, too. You can search for a branch near you using the company’s locator or can request a call online. We never like seeing a bank that requires an online form to see any application process information — Citibank requiring a call request takes this a step further in the wrong direction. Having to wait for a call back instead of providing borrowing requirements and application process information online is a big drawback.

Again, you’ll also need to have a business bank account with Citibank before you can apply for one of their lending products.

| Sales & Advertising Transparency2.2 |

|---|

| Sales Practices 2.0 |

| Web Presence 2.5 |

Citibank is not as transparent as other banks. This lender makes it difficult to impossible to find concrete information on borrower qualifications, interest rates, fees, or application processes or timelines. It’s worth noting that Citibank is forthcoming with borrower amounts and term lengths.

| Customer Service2.8 |

|---|

| Personal Support 1.9 |

| Self-Service 5.0 |

You can reach out to Citibank’s customer service by phone, and extended customer service hours are available. You can also visit a local branch. However, for such a big company, we expect to see more support options. Citibank also receives some negative complaints regarding customer support.

| User Reviews2.1 |

|---|

| User Feedback 2.0 |

| Review Site Aggregate 2.1 |

If you’ve kept an eye on the news cycle over the last ten years, you’ll know that big banks have a bit of an image problem. Citi is no exception.

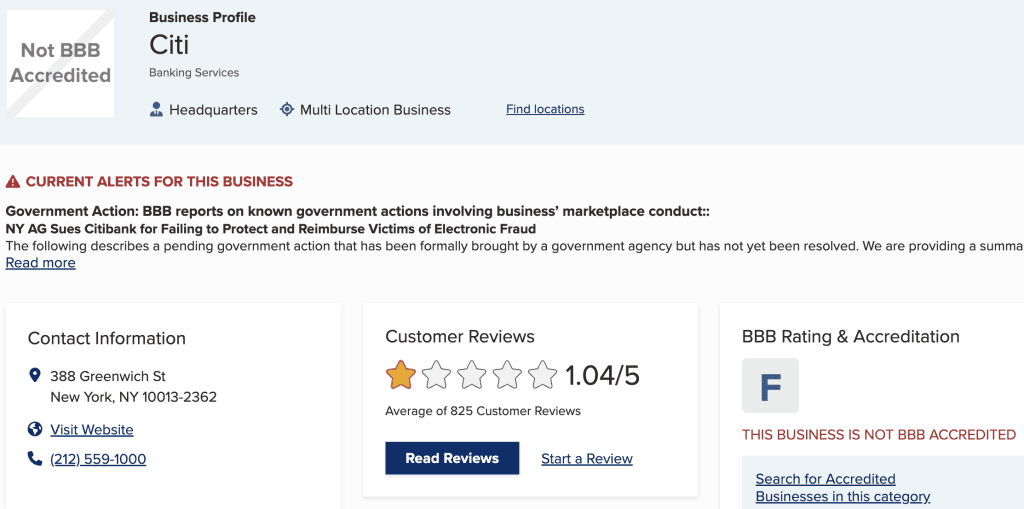

The bank receives a dismal F on BBB, with over 6,900 complaints closed in the last three years (a whole 1,000 more complaints since our last review). The company also has a current BBB alert regarding a lawsuit against Citibank for not protecting or reimbursing fraud victims.

Citibank fairs slightly better on some third-party review sites with an aggregate rating of 2.1/5 stars, but the sheer volume of negative reviews is troublesome. Granted, many of the complaints concern Citi’s credit card services, not its lending services, but the overall company reputation is still not great.

Source: BBB, screenshot captured 3/12/2024

Citi’s poor ratings are based on a variety of factors, ranging from failures to respond to complaints to government action against the bank. Specific issues with the bank include:

Are things sounding grim? Rest assured, there are still reasons to consider Citi for your business loan if you qualify:

Citibank’s size and wealth mean it can, in theory, offer businesses excellent rates on loans, but with hardly any information provided on the company’s site, there’s no way of proving this is true.

Compared to its competitors, even to other big banks, Citibank is an opaque lender, disclosing very little about its business lending products upfront. Combined with lingering customer service and legal issues plus a slew of negative reviews, this bank does not present the most friendly face to prospective borrowers.

Citibank is also behind the times in the business lending scene. Requiring business owners to visit a location for most application steps instead of providing an online option is almost unheard of nowadays.

If you need small business financing, you’d be better off checking other more reputable small business loans or small business line of credit options.

Merchant Maverick has been researching and reviewing business lenders since 2015. Our writers have tested over a hundred different funding products, including traditional term loans, online loans, lines of credit, start-up loans, merchant cash advances, and equipment financing. In each review, we evaluate rates and fees, services, eligibility requirements, application process, sales and advertising transparency, customer service, and user reviews.

Read more about how we rate business loans and funding products.

When comparing different lenders and loan products, we consider many data points, including the ease and transparency of the application process, interest rates, repayment structure, sales ethics, time to funding, revenue and time in business qualifications, and credit score requirements. Our lists of the best funding products include only those we’ve deemed worthwhile from multiple vantage points, and often share qualities such as widespread accessibility across fifty states, low rates, flexible requirements, and competitive borrowing amounts.

We spend an average of 10-15 hours researching and updating each one of our lists, making sure the loans and funding products included meet our internal standards for quality and reputation.

Find Funding for Any Credit Level

BusinessLoans.com  |

|---|

Explore a wide range of business loan options at BusinessLoans.com. With no minimum credit score requirement, find the perfect funding solution for your needs. Get Started.

Find Funding for Any Credit Level

BusinessLoans.com |

|---|

Explore a wide range of business loan options at BusinessLoans.com. With no minimum credit score requirement, find the perfect funding solution for your needs. Get Started.

Let us know how well the content on this page solved your problem today. All feedback, positive or negative, helps us to improve the way we help small businesses.

Give Feedback

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Our expert reviewers found BusinessLoans.com to have a quick and easy application process alongside excellent support and guidance for borrowers.

Start A Quick Application

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.

Our expert reviewers found BusinessLoans.com to have a quick and easy application process alongside excellent support and guidance for borrowers.

Start A Quick Application

"*" indicates required fields