U.S. Bank Business Banking Review

U.S. Bank offers a wide range of business services and is fully online and convenient for small businesses.

-

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

-

REVIEWED BY

Editor & Senior Staff Writer

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

U.S. Bank Business Banking

| Total Rating |

3.8 |

|---|---|

| Fees & Rates2.7 | |

| Services5.0 | |

| Rewards2.0 | |

| Features4.5 | |

| Eligibility Requirements5.0 | |

| Application Process4.0 | |

| Sales & Advertising Transparency3.3 | |

| Customer Service4.7 | |

| User Reviews2.7 | |

Monthly Fee Range

$0/month - $34/monthAPY Range

0.05% - 3.90%Account Types Offered

Checking, savings, CDs, and money market accountsU.S. Bank Business Banking At A Glance

- U.S. Bank offers numerous business services, supports cash deposits, provides free ATM access at its branches, and has over 2,000 physical locations.

- Its business services include checking and savings accounts, money market accounts, loans, merchant services, and payroll services.

- U.S. Bank’s checking accounts lack cashback or APY earning potential, but its money market accounts offer competitive APY rates.

Pros

- Wide range of business banking services

- Cash deposits supported

- Free ATM access at U.S. Bank ATMs

- Over 2,000 physical branch locations

- Competitive money market APY

Cons

- Large number of customer complaints

- Reports of account closures and payment issues

- High wire transfer and cash deposit fees

- Limited checking rewards

Table of Contents

- What Is U.S. Bank?

- Services Offered By U.S. Bank

- U.S. Bank Rewards & Perks

- U.S. Bank Fees

- U.S. Bank Eligibility Requirements

- U.S. Bank Application Process

- U.S. Bank Features

- U.S. Bank Sales & Advertising Transparency

- U.S. Bank Customer Service

- U.S. Bank Reviews & Complaints

- Is U.S. Bank Safe?

- Final Verdict: Is U.S. Bank Business Banking Worth It?

What Is U.S. Bank?

U.S. Bank is a traditional banking institution founded in 1863 that serves millions of customers nationwide.

U.S. Bank offers personal and business banking services, along with additional financial products like credit cards, wealth management, loans, merchant services, and payroll solutions. The company remains one of the largest banking institutions in the United States despite a significant number of customer complaints online.

U.S. Bank operates heavily throughout the Midwest and West Coast, with branch locations currently available in 26 states. Its banking services are also fully accessible online, so businesses do not need to be located near a physical branch to open and manage accounts.

Services Offered By U.S. Bank

| Services5.0 |

|---|

| Banking Services 5.0 |

| Online Portal & Mobile App 5.0 |

U.S. Bank offers a wide range of business banking and financial services, making it a strong option for businesses that want to manage multiple financial needs through one institution.

- Business checking accounts

- Business savings accounts

- Money market accounts

- Certificates of Deposits (CDs)

- Credit cards

- Corporate cards

- Business loans

- Lines of credit

- Merchant services

- Payroll services

- Legal services

- Fraud protection

- Gift cards

U.S. Bank also offers personal banking products for business owners who want to keep their personal and business banking with the same institution.

U.S. Bank Rewards & Perks

| Rewards2.0 |

|---|

| Quality & Value Of Earned Rewards 2.0 |

U.S. Bank’s rewards are less competitive than some of the top online business banking options. Its business checking accounts do not offer cashback rewards or APY, and its standard business savings account rates are relatively low compared to many online banks and fintech platforms.

However, U.S. Bank’s money market accounts offer more competitive APYs.

You can receive a bonus interest rate up to 3.90% from the account opening date when you open a new Platinum Business Money Market Account and complete qualifying activities, subject to certain terms and limitations. Member FDIC.

U.S. Bank also offers unique perks like the Business Savings Sweep account, which automatically transfers excess daily checking balances into savings.

Additional rewards and perks include:

- Welcome bonuses based on qualifying activities

- Discounts on check orders through U.S. Bank

- 0.05%+ APY on savings accounts

- Up to 3.72% APY on money market accounts

Interest is accrued daily and paid monthly on qualifying accounts.

U.S. Bank Fees

| Fees & Rates2.7 |

|---|

| Pricing 2.7 |

| Transaction Fees 2.0 |

| Transparency 5.0 |

When it comes to fees, U.S. Bank makes monthly account pricing relatively easy to compare, though some transaction fees can be difficult to locate and may require digging through the U.S. Bank knowledgebase.

A monthly fee may apply depending on which account you sign up for. Pricing is as follows:

| U.S. Bank Business Banking Plans | Price | When To Use |

|---|---|---|

| U.S. Bank Business Essentials | $0/month | If you want no monthly fee plan with up to 25 free teller and paper transactions and 25 cash deposit units each month |

| U.S. Bank Gold Business Checking Package | $20/month (waivable) | If you need 350 free transactions and 125 cash deposit units per month |

| U.S. Bank Platinum Business Checking Package | $30/month (waivable) | If you need 550 free transactions and 250 cash deposit units per month |

| Premium Business Checking Package | $34/month | If you have higher balances and more complex banking needs |

| Basic Business Savings Account | $5/month (waivable) | If you want a traditional business savings account and can meet the $500 minimum daily balance required |

| Business Savings Sweep Account | $45 - $70 | If you want an account that automatically moves excess checking balances into a U.S. Bank checking account |

Overall, U.S. Bank’s fees are somewhat higher than those of many online banks and fintech platforms, which is fairly common among traditional banks with physical branch networks. However, U.S. Bank’s wire transfer fees are among the highest we’ve seen in business banking, even compared to other traditional banks.

U.S. Bank also charges monthly maintenance fees on several accounts. While many of these fees are waivable, the requirements may be difficult for some businesses to meet.

If your business frequently sends wire transfers or cannot consistently meet fee waiver requirements, costs can add up quickly.

U.S. Bank does not charge ATM fees at U.S. Bank ATMs. However, out-of-network ATM fees may apply, and U.S. Bank does not clearly disclose all out-of-network ATM costs.

These fees apply to all U.S. Bank accounts:

| U.S. Bank Business Banking Category Fees | Value |

|---|---|

| Monthly Fee Range | $0/month - $34/month |

| Monthly Checking Fee | $0 - $34/month |

| Monthly Savings Fee | $5/month |

| ATM Fee | None |

| Overdraft Fee | $12.50 |

| ACH Fee | $1 |

| Incoming Domestic Wire Transfer Fee | $14 - $16 |

| Outgoing Domestic Wire Transfer Fee | $30 - $40 |

| Incoming International Wire Transfer Fee | $16 |

| Outgoing International Wire Transfer Fee | $75 |

| Wire Transfer Fee Start Point | $14 |

| Wire Transfer Fee Range | $14 - $75 |

| Cash Deposit Fee | Varies |

| Foreign Transaction Fee | 3% |

| Excessive Transactions Fee | Varies |

| Stop Payment Fee | $35 |

U.S. Bank Eligibility Requirements

| Eligibility Requirements5.0 |

|---|

| Eligibility Qualifications 5.0 |

| Eligibility Availability 5.0 |

| Eligibility Transparency 5.0 |

U.S. Bank’s eligibility requirements are relatively accessible compared to many traditional banks. The bank supports a wide range of business types, including sole proprietorships.

To apply online, applicants generally must own at least 20% of the business. Requirements may vary for in-branch applications.

U.S. Bank Application Process

| Application Process4.0 |

|---|

| Ease & Transparency Of Application 5.0 |

| Application Timeline 0.0 |

| Opening Deposit Requirements 5.0 |

Businesses can apply for U.S. Bank accounts online, by phone, or at a physical branch location.

U.S. Bank clearly outlines the information needed during the application process. Applicants will generally need to provide standard personal and business information, including an SSN or ITIN, TIN, and estimated or historical debit and credit card sales information.

Additional documentation may be required depending on the business structure, and most accounts require a $100 minimum opening deposit.

U.S. Bank does not publicly provide a timeline for how long the application and approval process typically takes.

U.S. Bank Features

| Features4.5 |

|---|

| Transaction Types Supported 5.0 |

| Transaction Limits 4.0 |

| Standard Banking Features 5.0 |

| Finance Management Features 4.5 |

| Extras 3.0 |

Traditional banks often offer a broader range of banking features and services than fintech platforms, and U.S. Bank is no exception. U.S. Bank offers a solid selection of business banking features, though some information can be difficult to locate because details are spread across multiple areas of the website.

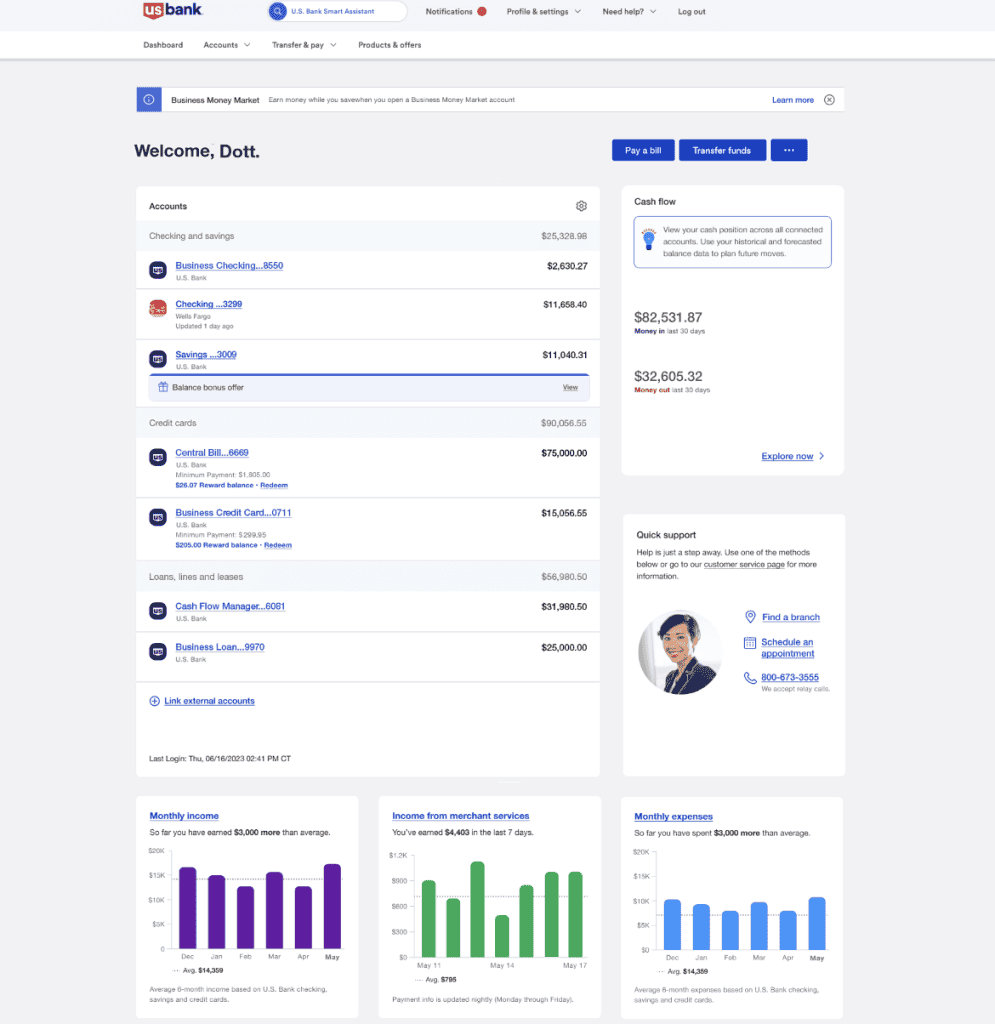

One standout feature is U.S. Bank’s online business banking dashboard simulator, which lets potential customers preview the platform before applying. The simulator even includes demonstrations of integrations and banking tools, which is a nice addition that many banks and fintechs do not currently offer.

Here is an overview of U.S. Bank’s business banking features:

| U.S. Bank Business Banking Features | Availability |

|---|---|

| Incoming Domestic Wire Transfers | |

| Outgoing Domestic Wire Transfers | |

| International Wire Transfers | |

| ACH | |

| ATM | |

| Cash Deposits | |

| Mobile Deposits | |

| Check | |

| Virtual Cards or Digital Wallet | |

| Bill Pay | |

| Cash Flow Management | |

| Reporting | |

| Standard FDIC Insurance | |

| Invoicing | |

| Accounting Integrations |

Businesses that use U.S. Bank for both personal and business banking can also easily switch between accounts within the platform.

U.S. Bank Sales & Advertising Transparency

| Sales & Advertising Transparency3.3 |

|---|

| Sales Practices 3.0 |

| Web Presence 4.7 |

U.S. Bank is relatively transparent overall, and its website avoids excessive marketing jargon and overly aggressive advertising language.

However, some information — particularly details related to fees and features — can be harder to locate than we would prefer, requiring users to navigate through multiple pages and support articles.

One area where U.S. Bank could provide more transparency is around its security practices and infrastructure protections, as publicly available information in these areas is somewhat limited.

U.S. Bank Customer Service

| Customer Service4.7 |

|---|

| Personal Support 4.0 |

| Self-Service 5.0 |

Customer reviews for U.S. Bank frequently mention inconsistent customer service experiences. While there are positive reviews from some customers, support quality appears to vary significantly between branch locations and support channels.

For online support, U.S. Bank does offer a large knowledgebase with helpful how-to articles, educational resources, and banking best practices that may reduce the need to contact customer service directly.

When support is needed, businesses can contact U.S. Bank through multiple channels. Support availability varies depending on the specific service and whether support is being provided online or through a physical branch, though many business banking services offer 24/7 phone support.

U.S. Bank Reviews & Complaints

| User Reviews2.7 |

|---|

| User Feedback 3.0 |

| Review Site Aggregate 2.6 |

Customer reviews for U.S. Bank are overwhelmingly negative overall. While the company maintains BBB accreditation and an A+ rating, there have been more than 2,000 complaints filed through the BBB in the last three years, in addition to complaints across other review platforms.

While customer reviews should always be viewed with some context, the volume and consistency of certain complaints stand out. Common concerns include unexplained account closures, long-pending transactions, difficulties resolving fraud claims, and inconsistent customer support experiences.

Negative U.S. Bank Reviews

- Poor customer support

- Unexplained account closures

- Long-pending transactions

- Issues receiving payment refunds

- Low spending limits

Positive U.S. Bank Reviews

- Helpful branch employees

- Wide variety of banking products and business services

- Easy deposits and transfers

Is U.S. Bank Safe?

U.S. Bank is an FDIC-insured traditional bank, which may provide some businesses with added confidence compared to newer fintech platforms that rely on partner banks.

The bank also offers fraud detection tools and educational resources covering cybersecurity best practices and fraud prevention.

However, publicly available information about U.S. Bank’s internal cybersecurity infrastructure and physical data center protections is somewhat limited compared to some competitors.

U.S. Bank does provide a detailed privacy policy outlining how customer data is collected and used.

Final Verdict: Is U.S. Bank Business Banking Worth It?

U.S. Bank is a well-established traditional bank that offers a wide range of business banking products and financial services, including checking and savings accounts, merchant services, payroll tools, loans, and credit cards.

Overall, U.S. Bank stands out for its broad selection of services, competitive money market APYs, extensive educational resources, and relatively accessible eligibility requirements. Sole proprietors and many other business types can qualify for accounts, and businesses that prefer traditional banking with physical branch access may appreciate U.S. Bank’s large branch network.

However, U.S. Bank’s rewards and APYs are less competitive than many leading online business banking platforms. The bank also charges relatively high wire transfer fees, and its cash deposit fee structure can be confusing compared to some competitors.

We also have to note two concerns: limited public transparency regarding some security infrastructure details and a large volume of negative customer reviews related to account closures, pending transactions, and customer support experiences.

That said, U.S. Bank’s long history and nationwide presence still make it a viable option for many businesses, particularly those already using U.S. Bank for personal banking or businesses that value branch access and a wide range of financial products.

If you’re still not sure if U.S. Bank is right for you, we recommend taking a tour of U.S. Bank’s unique dashboard simulator and seeing how U.S. Bank compares to our other top business savings accounts and top business checking accounts.

Chelsea Krause

Expert Contributor

Chelsea Krause is a writer who specializes in accounting, payroll, and small business loans. She has been helping small business owners manage their finances since 2016. She is a QuickBooks Certified User and former eCommerce store owner. Her accounting expertise has been quoted in Forbes and her work appears in Startup Nation, Small Business Bonfire, and Women on Business. Chelsea graduated summa cum laude with a BA in English & Creative Writing from George Fox University and studied abroad at the University of Oxford as well.

View Chelsea Krause's professional experience on LinkedIn.

Latest posts by Chelsea Krause (see all)

- TimeTrex Workforce Management Review - October 15, 2024

- eSmart Paycheck Review - October 15, 2024

- U.S. Bank Commercial Rewards Card Review - September 26, 2024

- U.S. Bank Business Banking Review - September 26, 2024

- Prime Alliance Bank Review - September 25, 2024