Best Mobile Credit Card Processing Apps

Read More

Oct 30, 2025

Filed under: Credit Card Processing, Mobile Payments

There are multiple ways businesses can accept credit card payments on a phone––but not all mobile payment types are affordable and safe. Read this guide to learn about the best mobile point of sale options.

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

REVIEWED BY

Expert Contributor

The best credit card processing companies enable small businesses to accept credit card payments on their phones. However, there are a few different ways to accept credit cards using a phone, including a mobile card reader, a virtual terminal, QR codes, payment links, and Tap to Pay.

This guide walks you through how to accept credit card payments on your phone, including a breakdown of mobile card reader options and step-by-step instructions on how to get started.

Table of Contents

Yes, you can accept credit card payments for your business using your phone and a payment processing service. This payment acceptance method is referred to as “mobile POS” and typically includes a mobile payment processing app that connects with a credit card reader.

The best mobile POS systems can also accept credit card payments on mobile phones without a credit card reader through the use of Tap to Pay, payment links, QR codes, or a virtual terminal.

Individuals can make and accept non-business credit card payments using peer-to-peer payment apps that don’t require a merchant account to set up, such as Cash App, PayPal, or Venmo. However, this method is different from and more limited than processing options available for businesses.

| Type Of Credit Card Reader | How It Works |

|---|---|

| Magstripe Readers | Reads code from a swiped card’s magnetic stripe; Least secure option |

| EMV Readers | Reads payment information from the EMV chip embedded in a card; Card inserted into the reader |

| NFC Readers | Payment data transmitted at close range; Contactless payments via smartphone or tap-enabled cards |

A mobile credit card reader is a plug-in or Bluetooth-enabled device that allows merchants to accept credit card payments on their phones.

The best credit card readers will incorporate two, or even all three transaction types: magstripe, EMV chip, and Near Field Communication (NFC) transactions.

Mobile credit card readers are usually provided by your existing merchant account provider or via a third-party processor/payment service provider, such as Square or PayPal.

Here’s a look at the types of mobile credit card readers and how they work.

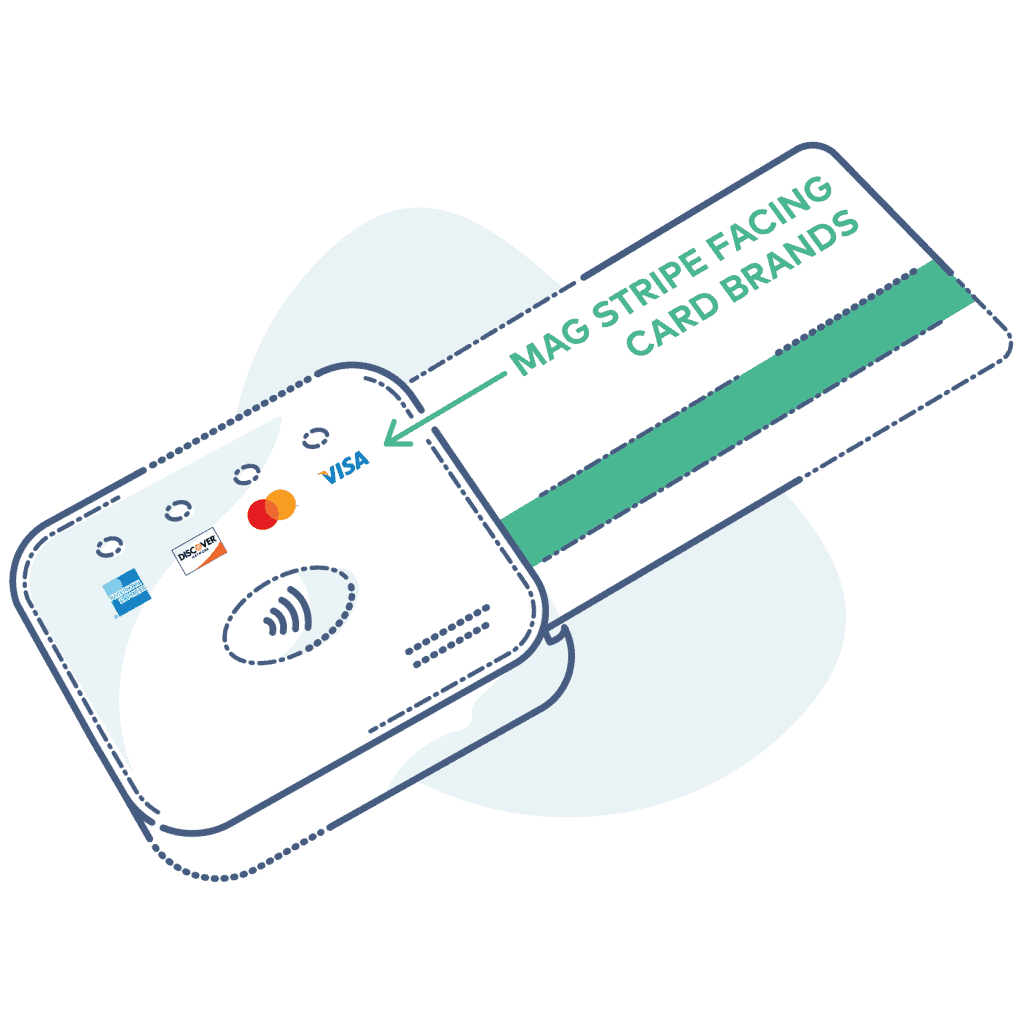

A credit card swiper accepts magnetic stripe (magstripe) payments — the type of payment credit cards were originally designed for. While they are convenient and possess a smaller physical profile compared to other types of readers, they are becoming nearly obsolete.

Of the three methods of accepting credit card payments, magstripe payments are by far the least secure. What’s more, due to regulations enacted in 2015, if a merchant only has a magstripe reader and a customer uses a stolen or fraudulent card with both a magstripe and a chip, the merchant is responsible for the loss on the purchase.

To shift the liability back to the credit card companies, the merchant needs to have an EMV or NFC card reader.

EMV card readers are colloquially known as chip card readers. With EMV technology, your payment information is stored digitally on a square chip embedded in your card.

As EMV is designed to be much more secure against fraud than magstripe technology, anybody doing business in the modern world will want to be able to accept EMV payments to help prevent chargebacks.

NFC stands for Near Field Communication, and it refers to wireless payment technology that transmits payment information at close range. NFC payments are sometimes referred to as contactless or tapped payments.

Customers can use digital wallets such as Apple Pay, Google Pay, and Samsung Pay to transmit their payment information via their smartphone or smartwatch. Alternatively, they can pay with an NFC-enabled credit card. Unlike magstripe technology, contactless payments are highly secure.

However, contactless NFC technology is not yet as widely used as EMV and magstripe technology in the US, so if you choose to accept NFC payments, you’ll want to be able to accept other types as well.

Thankfully, most mobile card readers that can accept contactless payments can also accept chip (EMV) and/or swiped (magstripe) payments.

To accept credit card payments on your phone, you’ll need to choose which payment acceptance method you’ll be using, sign up with a processor, and go through an app onboarding process. Here’s how to accept payments on a mobile phone:

| Acceptance Method | How It Works |

|---|---|

| Mobile Credit Card Reader | A small payment reader that is plugged into a mobile device’s headphone jack or charging port, or connected via Bluetooth. Can use magstripe, EMV, and/or NFC technologies. |

| QR Code | Scannable 2D barcode is generated with a POS app. Customers scan the code with their phone and are prompted to securely pay via credit card or mobile wallet. Businesses can also scan customer QR codes to accept payment. |

| Payment Link | Similar to a QR code, a payment link is generated for a specific transaction that prompts customers to securely pay online. Payment links may be texted or emailed to the customer. |

| Virtual Terminal | An online portal that requires the merchant to manually enter the customer’s credit card details. Slow, expensive, and relatively insecure—but can be good backup in the case of card reader failure. |

| Tap To Pay | A contactless payment technology that uses your smartphone’s NFC antenna to accept tapped payments without a card reader. Not offered by all payment processors or on all devices. |

As there are multiple ways to accept credit card payments using a phone, you’ll need to determine which method will be best for your business.

When choosing between a credit card reader, Tap to Pay, QR codes, payment links, or a virtual terminal, you’ll need to consider security, speed, and compatibility.

Some apps offer several options for processing a credit card transaction, so you may not need to choose just one.

If you want to start processing payments with your mobile device, you’ll need an account with a payment processor. This can be a traditional merchant account from a merchant services provider or an aggregated merchant account from a PSP (i.e., not a full merchant account).

When choosing a payment processor, you’ll need to ensure that their hardware and software are compatible with the mobile device you are planning on using to accept card payments.

Generally, credit card readers are only available for use by established businesses or nonprofits, so you’ll need to have relevant information (such as your business’s EIN) on hand if you’re signing up for the first time.

Most mobile POS services utilize an app or web app to process transactions. Make sure it’s opened, and you’re logged in.

If you’re signing up with these services for the first time, you’ll need to create an account and go through the setup process.

Each app’s setup process will be a little different, but they should allow you some customization, such as tips, receipts, and customer loyalty program signups.

Logging in with your password is just one security measure you should take when accepting credit card payments with your phone.

Adding extra layers of security, such as biometric locks, alphanumeric passwords, one-time passcodes, hardware keys, and other multi-factor authentication options, is always a good idea.

Customers may also need to approve their transactions, so be sure to include options for collecting signatures or PIN entries.

This step will vary somewhat depending on your payment processing service, but the basics of processing a transaction on your phone are as follows:

If your business operates in a field that is typically limited to cash payments, accepting card payments via phone is a great way to beat out your competition just by offering customers a more convenient way to pay.

For example, selling at a farmer’s market and advertising that you accept card payments can draw tons of customers in this age of increasingly non-cash payments.

So, be sure to put up signs that alert your customers to your business’s new payment options.

Accepting credit card payments on your phone can benefit both your business and customers, but it’s essential to decide which type or types of mobile payment work best for your business. When possible, businesses should try to use card-present processing methods, as the transaction fees are lower and the transactions are less susceptible to fraud.

Nevertheless, card-not-present payments (keyed-in and online payments) can still be useful for accepting mobile credit card payments when the customer is not physically present, or in the event that your card reader fails.

Fortunately, many processors offer free mobile card readers, so you can keep hardware costs down. Tap to Pay is another card-present payment option that eliminates the need to purchase a card reader.

In short, accepting credit card payments with your phone is usually a good move that won’t break the bank, but will likely draw in customers.

Get Your Free Credit Card Reader

Square |

|---|

Square is an industry-leading point-of-sale and payment processing provider. Sign up for a free account and get a complimentary card reader for use with Square POS. Start For Free.

Get Your Free Credit Card Reader

Square |

|---|

Square is an industry-leading point-of-sale and payment processing provider. Sign up for a free account and get a complimentary card reader for use with Square POS. Start For Free.

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.