Top Processors. Exclusive Rates. That's Maverick Match.

Answer a few questions about your business and get personalized payment processor recommendations paired with discounted partner rates you won't find anywhere else.

Get MatchedBank Of America Merchant Services has undergone many welcome changes in the past two years, including no more long-term contracts and predictable flat-rate pricing.

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

REVIEWED BY

Expert Contributor

| Total Rating |

4.0 |

|---|---|

| Fees & Rates4.1 | |

| Products & Services3.8 | |

| Contract4.6 | |

| Sales & Advertising Transparency3.8 | |

| Customer Service3.5 | |

| User Reviews3.0 | |

Table of Contents

Bank of America Merchant Services (BAMS) is the merchant services division of Bank of America (BofA), and one of the largest payment processors. BAMS offers an array of merchant services, including credit card processing, processing hardware, and support for eCommerce businesses.

The company now advertises merchant accounts that come without long-term contracts and no early termination fees (a vast improvement over its previous contracts through Fiserv/First Data which it recently split from).

With its completely revamped product lineup and more flexible contract terms, Bank of America Merchant Services appears to be moving in a positive direction. Is this enough to place it among the best credit card processing providers? Read on to find out.

| Products & Services3.8 |

|---|

| Software & Services 4.3 |

| Hardware & Equipment 3.2 |

Bank Of America Merchant Services earns solid scores in the Products and Services category, though these marks could be higher if BofA disclosed more information about its eCommerce services.

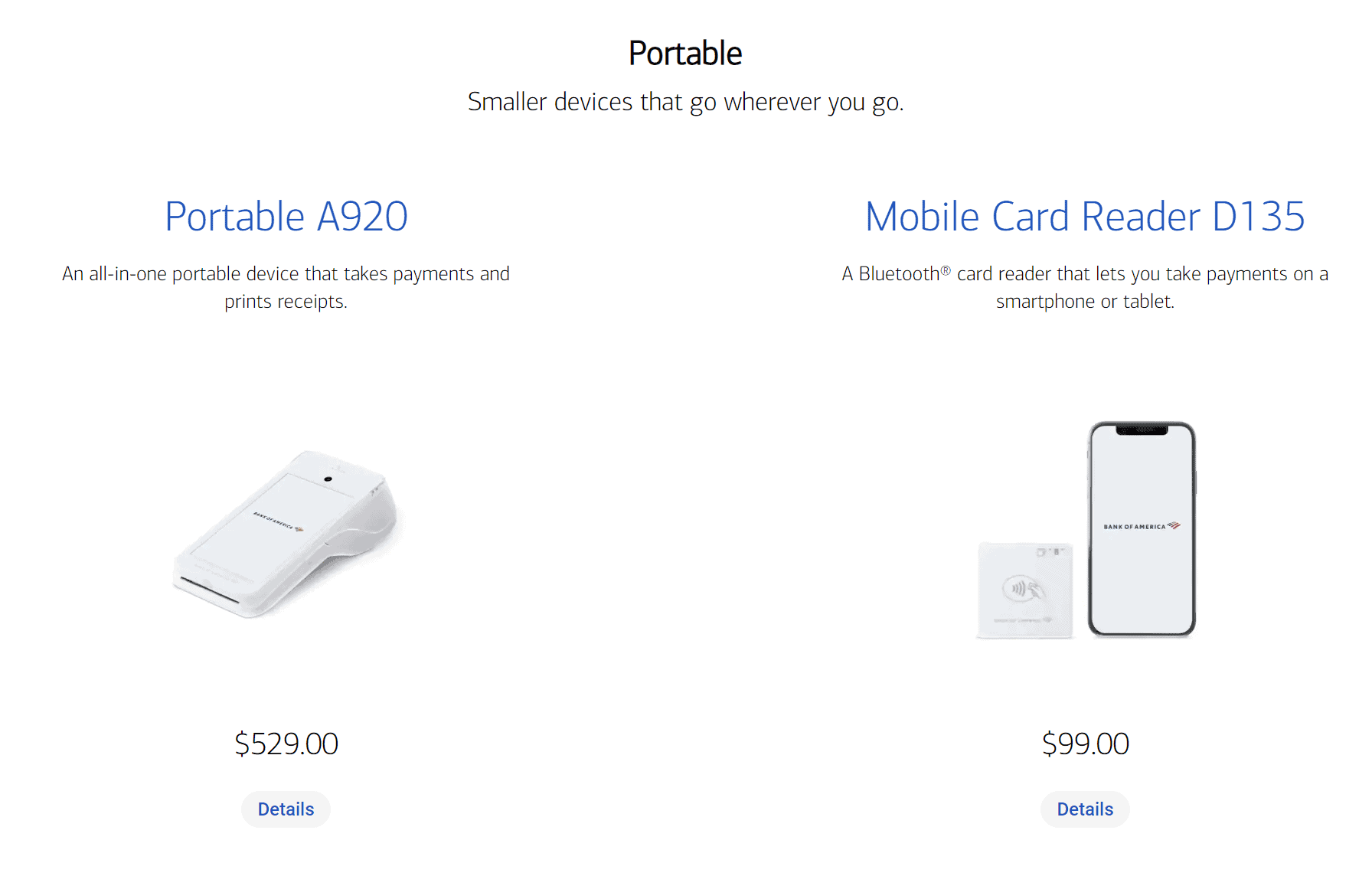

BAMS provides a full line of products and services for retail, eCommerce, and omnichannel businesses, including the following key features:

| Fees & Rates4.1 |

|---|

| Pricing 5.0 |

| Affordability 3.2 |

BAMS offers flat-rate credit card processing fees for small businesses, with processing rates fully disclosed on its website. Customized, quote-based pricing is also available if you ask for it. Overall, BofA’s solid score in this category disclosed rates are in line with industry averages, and we appreciate the transparency shown. The flat rates are slightly higher than those of Square, however.

| Sales & Advertising Transparency3.8 |

|---|

| Sales Practices 4.4 |

| Web Presence 2.9 |

BAMS earns a respectable score in this category, as the company has been heading in the right direction regarding disclosures of fees and other aspects of its merchant account services. There’s still room for improvement, however — particularly regarding its ancillary fees and its eCommerce offerings.

Bank of America Merchant Services has recently redesigned its website from the ground up, and it’s a tremendous improvement over the old one. The new site features extensive pricing disclosures, including processing rates for merchants on a simplified pricing plan and prices for the company’s many card readers, terminals, and peripherals.

However, there’s very little information about recurring or incidental fees, other than a footnote mentioning that POS systems require a monthly subscription fee and a vague claim of “no hidden fees.”

BAMS continues to use an in-house sales team to market and set up its accounts, which should lead to a positive sales experience in most cases. The company does state on its website that you will be presented with a complete fee schedule and all relevant contract documents and that you’ll be allowed to review them before signing up for an account. We strongly encourage you to thoroughly read all of your contract documents and clarify any lingering questions with your sales agent before signing up.

While the BAMS website includes links to all of the major social media sites, these accounts are for the main Bank of America organization, and finding information relevant to merchant services on any of them is quite challenging.

| Contract4.6 |

|---|

| Commitment 5.0 |

| ETF & Other Fees 4.2 |

BAMS prominently advertises on its website that its merchant accounts come with no long-term contracts and no early termination fees (ETFs). This is a welcome change from its previous practices when it was primarily a reseller for Fiserv, where three-year contracts and expensive cancellation penalties were the norm. Accordingly, BAMS now earns a great score in this category.

Note that there are still plenty of older online complaints from merchants who had to pay an ETF, but this appears to only apply to merchants whose accounts were underwritten by Fiserv prior to 2020.

We have yet to see any recent complaints from merchants regarding long-term contracts or early termination penalties, so we’re inclined to believe that BAMS is being honest about its contracts. Nonetheless, we strongly encourage you to read your contract documents thoroughly before signing up. BAMS doesn’t advertise any “free terminal” offers on its site, but it’s become common practice in the payments industry in recent years to pressure merchants to accept a free terminal in exchange for signing up for a long-term contract.

| Customer Service3.5 |

|---|

| Personal Support 3.8 |

| Self-Service 3.2 |

Like other aspects of BAMS’ services, customer support has been extensively revamped in the wake of the company’s split from being a Fiserv reseller to running an independent merchant services organization. Overall, these changes appear to be positive, leading to BAMS receiving a decent score in this category.

| Bank Of America Merchant Services Customer Service | Availability |

|---|---|

| Phone Support | |

| Email Support | |

| Support Tickets | |

| Live Chat | |

| Dedicated Support Representative | |

| Knowledge Base or Help Center | |

| Videos & Tutorials | |

| Company Blog | |

| Social Media |

True 24/7 phone and email support are now available, and you won’t have to contact a third-party partner to get help. At the same time, there’s still no live chat option.

Perhaps the biggest improvement is the launch of a new Merchant Help Center, an extensive online knowledgebase full of technical support discussions, product documentation, and other helpful resources. The Help Center includes a search function, which should make it easier to find the specific information you’re looking for.

The real question is how good the quality of BAMS’ customer service is, and at this point, we don’t have adequate feedback from merchants to assess this area. The company previously received many complaints from users alleging poor or ineffective customer support, but now that BAMS is handling this critical function in-house, we’re hopeful that it will lead to improvements in this area.

| User Reviews3.0 |

|---|

| Customer Feedback 3.0 |

| Review Site Aggregate 3.0 |

Merchant feedback regarding the current iteration of BAMS is quite hard to come by. At the very least, the complaint volume has dropped, but positive feedback is nearly nonexistent as well. BAMS’s user review rating reflects this ambiguity.

Since splitting with Fiserv/First Data in 2020, Bank of America Merchant Services has taken several positive steps to improve both the quality of its services and its reputation among merchants. It’s done away with long-term contracts, eliminated early termination fees, and introduced a flat-rate pricing plan with no monthly fees. It’s also instituted 24/7 customer support and completely revamped its hardware lineup, eliminating Clover products and replacing them with universal devices that can be reprogrammed if necessary.

Plus, while we can’t say for certain that BAMS has completely eliminated terminal leases, it’s clearly moved away from them by disclosing the prices for buying them outright.

These are all very welcome changes, especially in an industry where the biggest players tend to offer the worst services and pricing to small business owners.

While we have lingering concerns about the quality of the company’s customer service and are still waiting for more recent feedback from merchants to determine how these changes have actually improved the overall user experience, we’re comfortable with stating that BAMS has made some major improvements over the past few years.

If you’re already a Bank of America customer (or are willing to become one), it’s definitely worth your time to check out Bank of America Merchant Services and compare what it has to offer against other providers.

Credit Card Processing With Superior Support

Helcim |

|---|

With Helcim, you get everything you need to accept credit card payments online or in-person with a free account, plus high-quality support from real humans. Start For Free.

Credit Card Processing With Superior Support

Helcim |

|---|

With Helcim, you get everything you need to accept credit card payments online or in-person with a free account, plus high-quality support from real humans. Start For Free.

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.