Everything You Need To Know About Using A Credit Card Imprinter

Read More

Aug 22, 2024

Filed under: Credit Card Processing, Hardware, Point of Sale

? Save money on credit card processing with one of our top 5 picks for 2026

The best credit card machines make it easy to accept payments, track sales, and manage transactions from one device.

WRITTEN & RESEARCHED BY

Editor & Senior Staff Writer

Last updated onUpdated

REVIEWED BY

Expert Contributor

We reviewed top credit card machines based on payment method support, reliability, ease of use, POS features, processor compatibility, reporting tools, and overall value. Here are our top picks.

Answer five questions about your volume, ticket size, and industry, and we’ll rank these processors for your business.

| Provider | Best For | Price | Financing | Next Steps |

|---|---|---|---|---|

| Best For Low-Cost POS Features | $899 | $44/month | ||

| Best For Low-Volume Retailers | $299 | $27/month for 12 months | |

| Best Compact Countertop POS | $849 | $45/month | ||

| Best Full-Featured Mobile Terminal | $749 | $40/month | ||

| Best Low-Cost Smart Terminal | $349 | $32/month for 12 months |

Best For Low-Cost POS Features

Square Register is a solid pick for businesses that want an all-in-one countertop POS with Square’s built-in payment processing.

Square Register includes dual displays, Square POS software, Wi-Fi and Ethernet connectivity, and support for chip, swipe, tap, and mobile wallet payments. Businesses can also add compatible accessories and connect with Square tools for inventory, reporting, loyalty, appointments, and online sales.

Best For Low-Volume Retailers

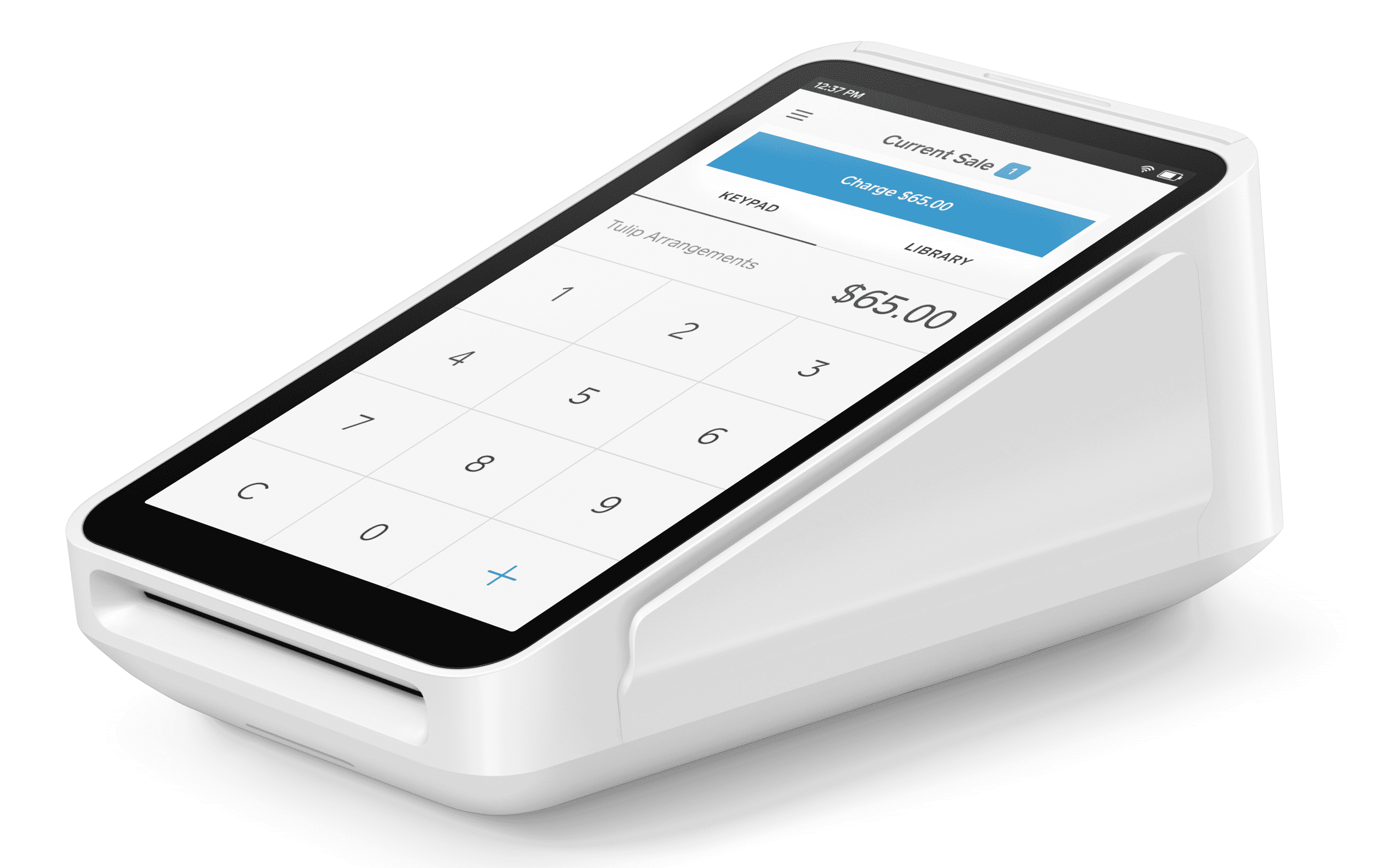

Square Terminal works well for low-volume retail businesses that want a compact payment terminal with more built-in functionality than a basic card reader.

Square Terminal includes a 5.5-inch touchscreen, built-in receipt printer, rechargeable battery, Wi-Fi, optional Ethernet through the Hub for Square Terminal, and support for chip, swipe, tap, and mobile wallet payments.

Best Compact Countertop POS

Clover Mini is built for businesses that want more POS functionality than a basic countertop payment terminal.

Clover Mini includes an 8-inch touchscreen, built-in receipt printer, PIN pad, Wi-Fi, Ethernet, LTE connectivity, and support for chip, swipe, tap, cash, check, and gift card payments. Businesses can also expand its functionality through the Clover App Market.

Best Full-Featured Mobile Terminal

Clover Flex is built for businesses that need a handheld payment terminal for sales on the floor, at the table, or in the field.

Clover Flex includes a nearly 6-inch touchscreen, built-in receipt printer, barcode scanner, Wi-Fi and LTE connectivity, and support for chip, swipe, tap, and mobile wallet payments. Businesses can also expand its functionality through the Clover App Market.

Best Low-Cost Smart Terminal

Helcim Smart Terminal is a great choice for businesses that want an all-in-one payment terminal with built-in POS tools and no required software subscription.

The terminal includes a 6.7-inch HD+ touchscreen, built-in receipt printer, Wi-Fi and 4G/LTE connectivity, inventory tools, employee PIN access, and support for tap, chip, PIN, and mobile wallet payments.

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.