PayPal Business Account Review

PayPal merchant services may not suit high-volume and high-risk businesses, but many sellers and customers will find PayPal easy and convenient.

-

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

-

REVIEWED BY

Expert Contributor

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

PayPal

| Total Rating |

4.2 |

|---|---|

| Fees & Rates3.8 | |

| Products & Services4.2 | |

| Contract4.6 | |

| Sales & Advertising Transparency5.0 | |

| Customer Service4.1 | |

| User Reviews3.3 | |

PayPal At A Glance

- PayPal offers businesses a vast commerce ecosystem that combines payment processing with eCommerce and mobile point of sale functionality.

- PayPal’s mobile point of sale app, PayPal Zettle, boasts an inexpensive card reader, an all-in-one touchscreen terminal, and transaction fees that are better for small-ticket merchants than PayPal’s online transaction fees.

- PayPal offers an expansive array of feature add-ons — both in-house tools and third-party integrations — along with developer tools that let you create your own.

Pros

- Trusted by consumers

- Good for low-volume merchants

- Extensive integrations

- Good developer tools

- All-in-one payments system

Cons

- Account stability issues

- Inconsistent customer support

- Not suitable for high-risk industries

- High fixed per-transaction fee hurts small-ticket merchants

Table of Contents

- What Is A PayPal Business Account?

- Countries Served By PayPal

- Supported Payment Types & Currencies

- Products & Services

- Funding Options For PayPal Business Account Users

- PayPal Integrations & Add-Ons

- Fees & Rates

- Sales & Advertising Transparency

- Contract Length & Early Termination Fee

- Customer Service & Technical Support

- User Reviews

- How Do PayPal Merchant Services Compare To The Alternatives?

- Final Verdict: Is PayPal Right For Your Small Business?

What Is A PayPal Business Account?

PayPal is universally known for its buy buttons and consumer digital wallet. However, for business users, as one of the largest payment processors available PayPal merchant services package offers robust tools that let you sell anywhere, anytime, and with no monthly fees for most basic services.

With numerous integrations on offer, you’ll have plenty of options for syncing PayPal with your current online store, accounting service, and/or shipping software. PayPal also provides its own mobile POS system, PayPal Zettle, which allows in-store PayPal payments. All in all, PayPal is one of the most comprehensive credit card processing packages in existence.

With its lack of contracts and no early termination fees, PayPal’s all-in-one business suite is a highly convenient tool for commerce. Sadly, PayPal’s fixed fee for online transactions hurts its value for small-ticket merchants. However, PayPal’s extensive functionality means that you’ll want to keep reading our PayPal business account review for the full story.

If you like what you see, we can help you set up a PayPal business account.

Countries Served By PayPal

You can use a PayPal business account in over 200 countries and territories worldwide. That’s nearly all of them, so if you’re reading this, the odds are strong that you can process payments with PayPal. However, not all of PayPal’s services and features are available everywhere. For example, PayPal Payments Pro is only available in the US, UK, and Canada.

Supported Payment Types & Currencies

Let’s take a look at the different payment types and currencies PayPal accepts.

Products & Services

| Products & Services4.2 |

|---|

| Software & Services 4.3 |

| Hardware & Equipment 4.0 |

PayPal earns a high score from us in the Products and Services category due to the sheer breadth and depth of its feature ecosystem along with the countless integrations available to fill any feature gaps. However, its POS system isn’t the most well-featured around, and large businesses may need more advanced customization than PayPal can provide.

| Feature | Availability |

|---|---|

| Payment Processing | |

| Dynamic Currency Conversion | |

| Recurring Billing & Subscriptions | |

| ACH Processing | |

| Invoicing | |

| Native POS & Card Reader | |

| eCommerce Integrations | |

| POS Integrations | |

| Mass Payouts | |

| Developer Tools | |

| Website Building | |

| Appointments & Reservations |

Before we delve into the full range of PayPal products, know that PayPal is a third-party processor (also known as a payment service provider (PSP) or an aggregator).

The main difference between a third-party processor and a traditional merchant account provider is that instead of giving merchants their own merchant account, PSPs aggregate all their merchants into one enormous merchant account. One unfortunate side effect of this arrangement is that merchants bear an increased risk of account instability. Holds and terminations are all too common due to the risk management policies required for PSPs to function.

On the plus side, the underwriting process for getting approved for an account is much less thorough than it is with a merchant account provider, putting them on our list of same-day merchant account providers that allow you to potentially be able to start accepting credit card payments the same day you apply for an account.

Our PayPal vs. merchant accounts analysis examines the whole scope of the differences between these two divergent payment processing methods.

PayPal Tools For Small Business

PayPal offers a huge number of business services under its payments umbrella. Here’s what PayPal provides for businesses beyond payment processing.

PayPal Zettle

PayPal’s Zettle mobile processing app is not the most feature-laden POS around, but it’s a solid choice for smaller sellers. It features a more robust inventory system and card reader than PayPal’s previous mPOS system, PayPal Here (which has since been deprecated and is no longer operable).

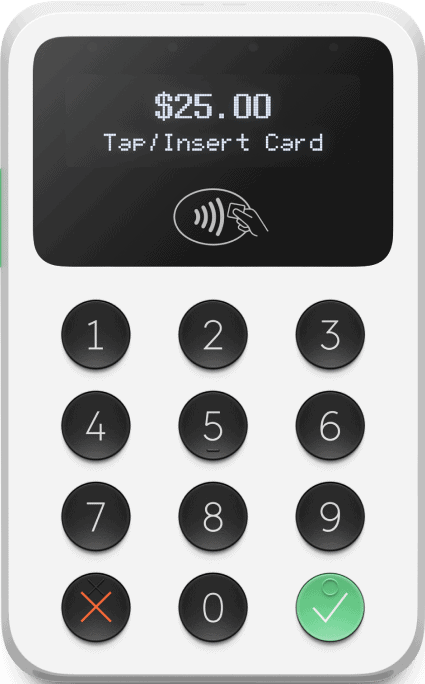

The fact that your funds get deposited into your PayPal account along with the rest of your online sales is pretty nice. You don’t have to pay any subscription or software fees; you just pay the processing costs. Plus, the Zettle Reader 2 is a handy little mobile card reader. Pair it with your smartphone or tablet, and it accepts chip card and NFC/contactless payments. Unlike many inexpensive mobile card readers, the Zettle Reader 2 has a PIN pad and a display.

The PayPal Zettle Reader 2

More recently, PayPal introduced the all-in-one Zettle Terminal, a device that combines the payment acceptance of the Zettle Reader with a touchscreen that runs the POS natively, eliminating the need to pair it with a smartphone or tablet.

The PayPal Zettle Terminal

Alternatively, Zettle allows merchants to use Tap to Pay on iPhone or Android to accept contactless payments without using any sort of card reader or terminal at all.

Funding Options For PayPal Business Account Users

Money from PayPal transactions is available almost immediately in your PayPal account. You can then spend that balance anywhere that accepts PayPal online or transfer the funds to your bank account. Standard next-day transfers typically take one to two business days and are cost-free.

If you need your funds within minutes, PayPal offers an instant transfer option. It will cost you 1.5% of the transfer volume, which is on par with what Square charges for the same service.

PayPal Integrations & Add-Ons

PayPal integrates with a vast number of software platforms, from online store builders to accounting applications, shipping tools, and email marketing software. There are just way too many to write out, but here’s a quick primer on the options available:

There’s a clear benefit to having so many integration options: You won’t have to worry about whether your shopping cart is compatible or not because it most likely is. The same goes for major accounting applications. Plus, there’s no shortage of well-known, robust POS solutions for retail stores and restaurants. PayPal also integrates with some more specialized solutions as well.

Fees & Rates

| Fees & Rates3.8 |

|---|

| Pricing 5.0 |

| Affordability 2.6 |

The fixed per-transaction fee charged by PayPal in nearly all circumstances is one of the highest such fees charged by any payment processor, bringing down PayPal’s rating in this category.

However, the fact that all PayPal core services come with no annual fee, no setup fee, no PCI compliance fees, and no cancellation fee helps mitigate this somewhat, as does PayPal’s complete pricing transparency.

Pricing Overview

| Item | Value |

|---|---|

| Pricing Starts At | $0 |

| Contract Length | Month-to-month |

| Processing Model | Flat-rate |

| Card-present Transaction Fee | 2.29% + $0.09 |

| eCommerce Transaction Fee | 2.99% + $0.49 for standard credit & debit transactions; 3.49% + $0.49 for PayPal & Venmo payments |

| Keyed-in Transaction Fee | 3.49% + $0.09 for keyed-in mobile & in-store transactions; 3.09% + $0.49 for virtual terminal transactions |

| Equipment Cost | $29-$199 |

The sheer number of different flat rates PayPal charges for payments under different circumstances makes the job of explaining PayPal’s pricing quite difficult. I’ve outlined PayPal’s fees below, but you can also check out our guide to PayPal’s credit card processing fees. This article explains PayPal’s pricing structure in finer detail.

Monthly Plans

| PayPal Plans | Price | When To Use |

|---|---|---|

| PayPal Checkout | $0/month | If you just want to add a PayPal button to your website. Can set up recurring billing if customer has a PayPal account. |

| PayPal Payments Advanced | $5/month | If you need customizable payment buttons and a hosted checkout. |

| PayPal Payments Pro | $30/month | If you need customizable payment buttons, a virtual terminal to manually key-in customers' card numbers, and a hosted checkout. |

In addition to the above, PayPal offers a special payment plan for enterprise-level businesses called PayPal Enterprise. This plan gives you access to a full Braintree merchant account and offers an optimized processing engine to remove friction at checkout, a brandable web portal, granular data analysis, and more.

Extra Costs

| PayPal Extra Costs | Price |

|---|---|

| Chargebacks | $20 per chargeback |

| International Transactions | 1.5% cross-border fee |

| Instant Transfers | 1.5% of the transfer amount |

| Recurring Billing | $10/month on Payments Advanced & Payments Pro plans |

| PayPal Payouts | 2% (max $1) using the online form, $0.25 per payout using the API |

| Micropayments | 4.99% + $0.09 per transaction |

| QR Code Transactions | 2.29% + $0.09 |

| Nonprofit Discount Rate | 1.99% + $0.49 per transaction |

PayPal sports a few more alternative rate offerings, including QR code transactions (processed via PayPal Zettle), a microtransactions plan, and nonprofit discounts. You’ll also need to pay incidental fees for things such as chargebacks and instant transfers.

Sales & Advertising Transparency

| Sales & Advertising Transparency5.0 |

|---|

| Sales Practices 5.0 |

| Web Presence 5.0 |

PayPal earns a perfect score in this category, as it is quite upfront with its sales and advertising. PayPal’s business rates — numerous as they are — are listed in plain sight, so there’s no hidden agenda. We also appreciate that PayPal does not use independent sales agents, who are prone to deceptive sales tactics.

However, don’t think that everyone can process with PayPal just because anyone can open an account. It’s just not true, and I think it plays a big role in complaints against PayPal. There’s a specific list of PayPal-prohibited businesses, which I encourage every prospective PayPal business account user to check out. You’ll also be under scrutiny as soon as you start processing. If PayPal decides you present an unacceptable risk, it will terminate your account.

You’ll want to understand how to prevent holds, freezes, and terminations if you go with PayPal (or any other PSP).

Contract Length & Early Termination Fee

| Contract4.6 |

|---|

| Commitment 5.0 |

| ETF & Other Fees 4.2 |

PayPal’s high score in this category reflects the fact that its merchant services are contract-free and have no early termination fee. Though this is standard with PSPs like Square and PayPal, we love to see this from merchant services providers.

The pay-as-you-go model is ideal if PayPal is your starter option, as you always have the option of upgrading to a merchant account later. However, if the rates work for you (particularly as just a secondary option), PayPal will also scale with your business.

Customer Service & Technical Support

| Customer Service4.1 |

|---|

| Personal Support 3.1 |

| Self-Service 5.0 |

PayPal’s marks in this category reflect the fact that the quality of PayPal’s live support, as reported by PayPal business users, is quite inconsistent. At the same time, we’ve taken into account the sheer number of 24/7 support options available and the comprehensive knowledgebase that reduces the likelihood that you’ll need live support in the first place.

| PayPal Customer Service | Availability |

|---|---|

| Phone Support | |

| Email Support | |

| Support Tickets | |

| Live Chat | |

| Dedicated Support Representative | |

| Knowledge Base or Help Center | |

| Videos & Tutorials | |

| Company Blog | |

| Social Media |

PayPal has many different customer service channels. Depending on your question or problem, any of these options may resolve the issues you might have:

- Community Forum: If you want insights and advice from other PayPal merchants, the community forum is a good place to start.

- Knowledgebase: PayPal’s self-help resources are pretty extensive, both for consumer users as well as merchants. You’ll find a vast array of questions and answers in the searchable database, which should cover most of your needs.

- Phone/Email: Any PayPal customer service review must note that PayPal’s phone support is quite inconsistent (see Negative PayPal Reviews & Complaints). Sometimes, you’ll get a rep who knows what they’re doing; other times, you won’t. Personally, when I tested the phone support, I had to wait a while for a callback, but I did ultimately receive helpful support. However, my advice is to avoid calling if possible. Between the knowledgebase, community forum, and quick answers sections, you should be able to find answers to the most common problems.

- Social Media: PayPal is active on Facebook, but if you want help on social media, you’re better off using Twitter/X. Send a tweet/whatever to PayPal, and you should get some assistance.

- Resolution Center: Through PayPal’s resolution center, you can communicate directly with a buyer to resolve a transaction problem. You can also use it to report unauthorized account activity, resolve an account limitation, and ask PayPal to investigate a transaction issue.

One compelling benefit of using PayPal is the sheer volume of users. Whenever you encounter an error or a problem, Google it, and the odds will be good that you’ll find a solution from another merchant who has already dealt with the same issue. However, when it comes to account issues such as funding holds, you’ll likely need to talk to someone over the phone.

If necessary, you can go through the BBB (read more about that in the User Reviews section).

User Reviews

| User Reviews3.3 |

|---|

| Customer Feedback 4.0 |

| Review Site Aggregate 3.0 |

PayPal’s score in this section accounts for the fact that user reviews of the company are very much a mixed bag. The greatest difficulty with quantifying negative PayPal account reviews is the fact that PayPal is also a consumer product. That means the vast majority of PayPal complaints come from consumers, not merchants.

Head to the website of the Better Business Bureau, and you’ll see an enormous number of complaints lodged and one-star user reviews. Likewise, PayPal’s average rating at Trustpilot stands at a dismal 1.8 out of 5, with the vast majority of consumer and business reviewers being negative.

However, PayPal’s public reception is much brighter at user review sites like G2 and Capterra, where PayPal earns excellent average scores of 4.4 and 4.7 out of 5, respectively.

How Do PayPal Merchant Services Compare To The Alternatives?

There are many alternatives to PayPal competing for your business. Let’s see how PayPal measures up against three of the best payment processors in the industry: Square, Stripe, and Helcim.

Final Verdict: Is PayPal Right For Your Small Business?

PayPal is a strong payment option for new businesses and is very convenient to use as a backup form of payment if you sell online. Of course, it functions quite well as your primary payment option as well. Setting up a PayPal business account is quick and painless; the platform is easy to use, it’s widely accepted, and consumers trust the brand name.

If you own a brand new business and need to accept payments quickly, PayPal is a good solution. Likewise, existing eCommerce merchants, including those selling internationally, have a truly impressive array of robust selling tools with PayPal. For in-person sales, while PayPal’s tools are simpler and less comprehensive than its online sales ecosystem, its processing rate is actually more competitive.

That said, as your business grows and you exceed $10K in monthly revenue, it may be more worthwhile to pursue a traditional merchant account because the processing costs will be lower, plus you’ll enjoy more account stability.

PayPal’s high fixed per-transaction fee for online sales negatively impacts the same small-ticket sellers that stand to gain the most from the platform, and we can’t ignore that. Nonetheless, the supreme ease and convenience with which you can start selling with PayPal and the genuinely impressive range of robust features at your disposal make it a solid processing choice for a wide variety of businesses.

Need more options? Check out our list of the best small business credit card processing companies.

Jason Vissers

Expert Contributor at Merchant Maverick

Jason has been writing about small business software platforms, services, and financing since 2015. Jason’s expertise has been featured in Yahoo Finance, Time/NextAdvisor, Home Business Magazine, CreditCards.com, GoBankingRates, TheLadders.com, and other publications. He has a bachelor’s degree in Political Science from San Diego State University.

View Jason Vissers's professional experience on LinkedIn.

Latest posts by Jason Vissers (see all)

- How Much Are Online Payment Processing Fees? - March 14, 2024

- How To Choose A Credit Card Reader - November 3, 2023

- Types Of Credit Card Readers - November 3, 2023

- How A Business Can Benefit From A Credit Card Reader - November 3, 2023

- Do Credit Card Readers Have Fees? - November 3, 2023

To learn more about how we score our reviews, see our Credit Card Processor Rating Criteria.