Stripe Payments Review

What is Stripe and is it legit? Stripe is a powerful tool for businesses that want to sell online, but is it a quality product at a fair price? Read our full Stripe review to find out.

-

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

-

REVIEWED BY

Expert Contributor

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

Stripe Payments

| Total Rating |

4.7 |

|---|---|

| Fees & Rates4.7 | |

| Products & Services4.5 | |

| Contract5.0 | |

| Sales & Advertising Transparency5.0 | |

| Customer Service4.5 | |

| User Reviews4.1 | |

Stripe Payments At A Glance

- Stripe’s massive eCommerce platform provides a strong alternative to PayPal

- Stripe’s developer support and ecosystem are among the best in its class, though this comes with a tradeoff in user-friendliness for non-programmers

- If you’re looking to dabble in international sales, Stripe has excellent support for foreign payment methods and currencies

Pros

- Excellent developer tools

- Predictable flat-rate pricing

- Advanced reporting tools

- Ideal for international merchants

- Excellent marketplace tools

- Exceptional subscription tools

- Multicurrency support

Cons

- Account stability issues

- Not suitable for high-risk industries

- Needs technical skills to implement

Table of Contents

What Is Stripe?

Stripe is among the most popular eCommerce payment processing services and has developed a reputation for innovation, predictable pricing, versatility, international commerce, and developer-focused resources. In fact, we ranked it as one of the best credit card processors for small businesses.

In its white-label form, Stripe provides payment processing for platforms such as Shopify and WooCommerce.

Products & Services

| Products & Services4.5 |

|---|

| Software & Services 5.0 |

| Hardware & Equipment 4.0 |

How does Stripe work, and what does it offer in the way of products and services for small businesses?

Stripe’s features are designed to be a modular toolset that can be adapted to a variety of eCommerce needs. In addition to payment processing, you’ll find invoicing, customer management, and advanced security tools.

You can also utilize Stripe’s prebuilt payments page, Stripe Checkout, which offers most of the basic functionality you need, along with the ability to customize its look with your brand.

| Stripe Payments Features | Availability |

|---|---|

| Dedicated Merchant Account | |

| PCI Compliance | |

| High-Risk Accounts | |

| International Accounts | |

| Contactless Payments | |

| ACH Processing | |

| Digital Wallet Acceptance | |

| EBT Acceptance | |

| Virtual Terminal | |

| Mobile POS Reader & App | With Stripe Terminal (requires programming experience) |

| Hosted Online Store | Hosted payment pages (not a fully featured store) |

| Payment Links | |

| Payment Gateway Integrations | Stripe is its own payment gateway. |

| Shopping Cart Integrations | |

| POS Integrations | With Stripe Terminal (requires programming experience) |

| BNPL Integrations | |

| API Documentation | |

| Currency Conversion | |

| Recurring Billing | |

| Invoicing | |

| Cash Discount Program | |

| Cryptocurrency Processing |

Below are some further details about Stripe’s more notable features. Get started with Stripe Payments.

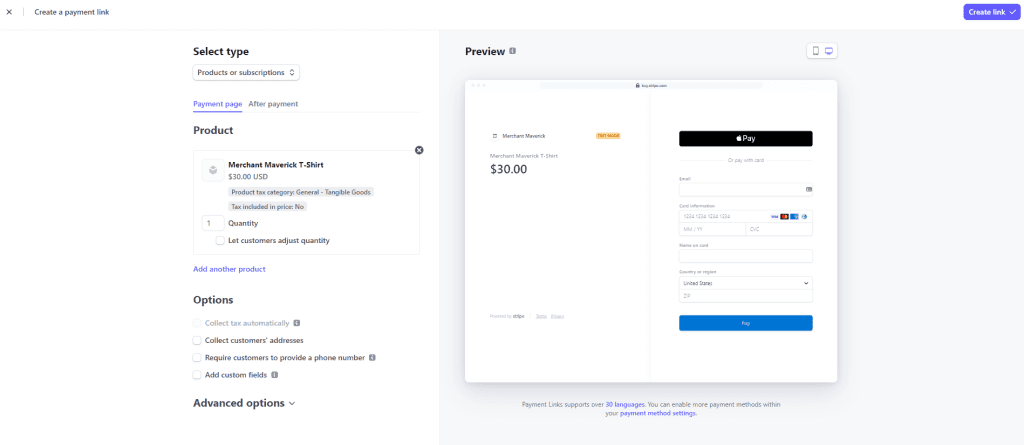

Stripe Payment Links

Payment links provide an alternative way to check out your customers by sending them a link by text, email, or messaging service. While this feature doesn’t require code to implement, you can use an API provided by Stripe to generate payment links programmatically. Checkout pages can be customized to reflect your branding aesthetics.

Note that payment links are distinct from billing/invoicing, as it only sends a link to checkout.

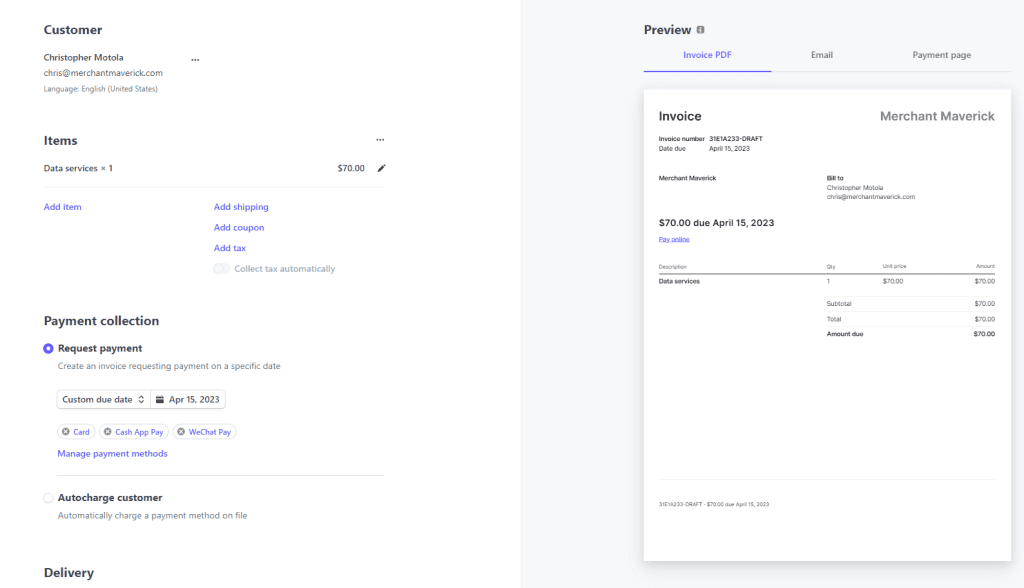

Stripe Invoicing

You can use Stripe Invoicing to send invoices globally. Invoices can be created through the Stripe dashboard without having to do any coding, however, as this is Stripe we’re talking about, you can use the Invoicing API to automate various aspects of the invoicing process.

Invoice parameters can be customized to your needs. You’ll be able to set your own icons and logos in JPG or PNG format (512kb in size and greater or equal in size to 128px by 128px). Brand colors and accent colors can also be set.

Other Stripe Business Management Tools

As a payment platform, Stripe offers tools aimed at helping customers manage their businesses. These services are aimed at businesses of different sizes, so you can opt-in as necessary.

Offerings include:

- Data Warehousing: You can centralize your Stripe-related data and reports through Stripe’s partnerships with Snowflake or Amazon Redshift.

- Stripe Financial Connections: This service verifies bank account information for ACH transactions and can be used to verify balances and minimize fraud in bank-to-bank transfers.

- Stripe Sigma: Sigma is Stripe’s advanced, SQL-powered reporting system. Businesses seeking deeper insight into their payment trends. Pricing scales with volume, so businesses of any size can theoretically use it.

- Stripe Atlas: Stripe Atlas is a service designed to help entrepreneurs form companies and startups. It can be used to form legal entities, issue stock to founders, and, of course, process payments.

- Stripe Climate: Stripe Climate is a service aimed at helping businesses access carbon-removal technologies.

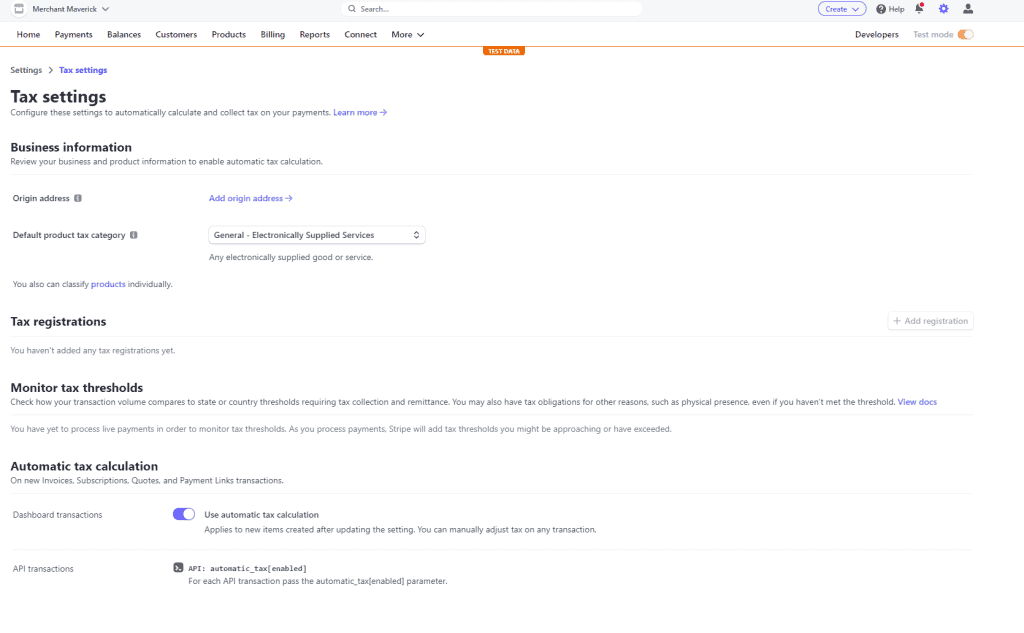

- Stripe Tax: Stripe Tax automates tax collection on your account. Keep in mind this applies not only to US taxes but also VATs and similar taxes in international markets.

- Stripe Revenue Recognition: Stripe Revenue Recognition is a service aimed at helping ease growing businesses’ accrual accounting needs.

- Stripe Identity: Another security tool for verifying user identity. It supports IDs from 33 countries.

Fees & Rates

| Fees & Rates4.7 |

|---|

| Pricing 4.4 |

| Affordability 5.0 |

Stripe Payments uses a flat-rate pricing system with transparent transaction fees, affordable hardware for in-person transactions, and no monthly fee—unless you need advanced tools or features like a custom domain.

Pricing Overview

| Item | Value |

|---|---|

| Pricing Starts At | $0/month |

| Contract Length | Month-to-month |

| Processing Model | Flat-rate |

| Card-present Transaction Fee | 2.7% + $0.05 |

| eCommerce Transaction Fee | 2.9% + $0.30 (2.2% + $0.30 for nonprofits) |

| Keyed-in Transaction Fee | 3.4% + $0.30 |

| Equipment Cost | $59-$349 |

Stripe’s pricing system is convenient for small businesses with limited transaction volumes but may become costly for growing businesses (unless they negotiate custom pricing). Not-for-profit organizations can boost their fundraising with Stripe’s nonprofit discounts.

Extra Costs

| Stripe Payments Extra Costs | Price |

|---|---|

| ACH Direct Debit | 0.8% per transaction ($5 cap) |

| International Cards | 1.5% |

| Currency Conversion | 1% |

| Chargeback Fee | $15 |

| Affirm | 6% + $0.30 |

| Klarna | 5.99% + $0.30 |

| Afterpay | 6% + $0.30 |

| Localized Payment Methods (From Outside Region) | 1.5% + variable transaction fee |

| Tap To Pay Transactions | +$0.10 |

| Invoicing | 0.4% per transaction |

| Instant Payouts | 1.5% ($0.50 minimum) |

Advanced features and international transactions have additional costs per transaction. You will also encounter incidental fees such as chargeback fees and fees specific to buy now-pay-later (BNPL) transactions.

Monthly Plans

| Stripe Payments Plans | Price | When To Use |

|---|---|---|

| Custom Domain | $10/month | If you want to use your own domain for customer-facing surfaces hosted by Stripe. |

| Billing | $620+/month (1 year contract) | If you need recurring revenue solutions such as subscription billing or a customer portal with self-managed plans. |

| Tax | $90/month (1 year contract) | If you need to automate tax calculation and collection on all your transactions. |

| Sigma | $10+/month | If you want to analyze your Stripe data using SQL. |

Some advanced tools, such as recurring billing, carry a monthly fee rather than a per-transaction fee. Generally, only larger businesses would use Stripe features requiring a monthly plan.

Stripe Payouts & Funding Times

- First Payout After First Transaction: Seven+ days

- US, Standard: Two business days

- High-Risk Businesses: 14 calendar days

- International Businesses: Varies by country 2-30 days

Stripe offers two-day payouts to most US-based merchants, except those it deems “high risk.” However, most international merchants will encounter longer funding times, all based on which country they’re in. While a waiting period of two business days is pretty standard across the industry, you can get faster payouts from some merchant account providers as well as Square.

Instant payouts are available for an additional charge (see Extra Costs table).

Countries Served

Stripe’s international reach is steadily growing. Stripe is readily available in most of the 47 countries below, though in a few cases, you’ll have to request an invitation to join the platform. This is usually a temporary restriction while Stripe is rolling out the service to new markets.

Be aware that new features will deploy in different countries at different times.

For example, Stripe Terminal has been available in the US for a while, but it was rolled out in Europe in 2022. Stripe supports local and universal payment methods from anywhere in the world by default but can be expanded to support international ones.

| Country | Availability | Country | Availability |

|---|---|---|---|

| Australia | Open | Lithuania | Open |

| Austria | Open | Luxembourg | Open |

| Belgium | Open | Malaysia | Open |

| Brazil | Open | Malta | Open |

| Bulgaria | Open | Mexico | Open |

| Canada | Open | Netherlands | Open |

| Croatia | Open | New Zealand | Open |

| Cyprus | Open | Norway | Open |

| Czech Republic | Open | Poland | Open |

| Denmark | Open | Portugal | Open |

| Estonia | Open | Romania | Open |

| Finland | Open | Singapore | Open |

| France | Open | Slovakia | Open |

| Germany | Open | Slovenia | Open |

| Gibraltar | Open | Spain | Open |

| Greece | Open | Sweden | Open |

| Hong Kong | Open | Switzerland | Open |

| Hungary | Open | Thailand | Open |

| India | Open | United Arab Emirates | Open |

| Ireland | Open | United Kingdom | Open |

| Italy | Open | United States | Open |

| Japan | Open | Indonesia | Invite only |

| Latvia | Open | Philippines | Invite only |

| Liechtenstein | Open |

Supported Payment Types & Currency

As a truly international product, Stripe supports a variety of payment types and over 135 currencies. Stripe’s supported payment methods are divided into two categories, universal and local.

Universal Payment Methods

Universal payment types are supported in all the countries where Stripe is available. These are:

- Alipay

- Apple Pay

- Google Pay

- Microsoft Pay

- Amex Express

- Mastercard

- Visa

- Discover

- Click to Pay

- Afterpay/Clearpay

- Klarna

Local Payment Methods

Local payment types are available by default within the regions the account is registered within, though it is possible to add support for foreign regions with additional coding and transaction costs (see Pricing above)

Currencies Supported By Stripe

Stripe supports too many currencies to list here, but you can find Stripe-supported currencies on the company’s website.

If you want to avoid exchange fees, you can specify “presentment” currencies when you set Stripe up. Stripe will accumulate separate balances for each currency you’re paid with, which it can then route to different bank accounts. If your presentment currency differs from the settlement currency, Stripe will automatically make the conversion for you, but this comes at an additional 1% fee. Note that exchange rates are subject to markups by financial institutions.

Sales & Advertising Transparency

| Sales & Advertising Transparency5.0 |

|---|

| Sales Practices 5.0 |

| Web Presence 5.0 |

Stripe is among the most straightforward and transparent payment processors out there, going so far as to exhaustively lay out its terms, conditions, and pricing publicly on its website. In fact, it’s so thorough that the handful of details that aren’t readily accessible and easy to find stand out a bit more. This mostly falls under the umbrella of non-standard pricing for nonprofits or high-volume businesses.

Despite the transparency, we’d recommend that you scrutinize Stripe’s pricing model, as it’s easy to pile on charges for advanced features if you aren’t careful. This won’t be due to a lack of disclosure, but rather the complexity of Stripe’s ecosystem.

Contract Length & Early Termination

| Contract5.0 |

|---|

| Commitment 5.0 |

| ETF & Other Fees 5.0 |

Is Stripe Honest & Transparent About Its Merchant Agreement?

In a word: yes. Just about everything you could possibly want to know about Stripe is researchable before you sign up for anything. While the platform can be complex, it is always transparent.

What Are The Commitments When You Use Stripe?

With the exception of a couple of specific advanced features, there are no commitments to make. Stripe is funded through your transaction fees. If your account isn’t doing anything, it doesn’t cost you anything.

How Easily Can You Terminate Your Agreement With Stripe?

No early termination fee. Period. Thumbs up because that’s what we like to see here. And remember, we said Stripe will help you export your customer data and take it with you if you ever decide to leave.

If you want to stop using Stripe, simply stop processing transactions with Stripe. You can keep your account dormant or formally close it from your dashboard. If you do the latter, you’ll need to deal with your remaining balances first.

Customer Service & Technical Support

| Customer Service4.5 |

|---|

| Personal Support 4.0 |

| Self-Service 5.0 |

Stripe offers extensive knowledgebases and developer references that are among the best in its class. Phone and email support are available and much improved over the past, although many merchants still report difficulty resolving freezes and holds.

| Stripe Payments Customer Service | Availability |

|---|---|

| Phone Support | |

| Email Support | |

| Support Tickets | |

| Live Chat | |

| Dedicated Support Representative | Premium |

| Knowledge Base or Help Center | |

| Videos & Tutorials | |

| Company Blog | |

| Social Media |

User Reviews

| User Reviews4.1 |

|---|

| Customer Feedback 4.0 |

| Review Site Aggregate 4.1 |

Negative Stripe Reviews & Complaints

Stripe has an A+ rating with the Better Business Bureau, with 1,352 complaints closed in the last three years. Stripe.com user reviews on the Better Business Bureau site include many complaints, with an aggregate customer review score of 1.02/5 (it’s quite common for BBB ratings to be very low).

Common complaints include the following:

Positive Stripe Reviews & Testimonials

Stripe has an expansive and impressive list of successful clients, including Shopify, WhatsApp, BMW, Google, Salesforce, Marriott, and Amazon. We’re talking about some major internet players, which constitutes a big deal — even though no specific praise is given besides their continued business.

Here are some reasons Stripe is popular.

Final Verdict: Is Stripe Worth It?

Without any doubt, Stripe Payments is one of the heavy hitters in the online payment processing sector, and for good reason. For low-risk businesses that have the technical acumen and the eCommerce focus, Stripe should definitely be on your shortlist. With no monthly account fees, you won’t be risking much to try it out, either.

While Stripe isn’t a perfect processor, it is an excellent one for eCommerce businesses that want global reach and powerful customizable tools. Ultimately, ask yourself two questions: (1) Will you use the tools Stripe has to offer? (2) Does Stripe have everything you need? If the answer to both questions is yes, it’s worth pursuing. If the answer to either question is no, you should consider some of Stripe’s competitors.

If you’re ready to give Stripe a try, check out our guide on creating a Stripe account.

Common Questions About Stripe Payments

Chris Motola

Expert Contributor at Merchant Maverick

Chris has been writing about small business topics since 2003. He has been featured in Fox Business, ABC News, Yahoo Finance, GoBankingRates, Newsweek, BizJournals, and other publications. He has a Bachelor’s of Arts in English Writing Arts from SUNY Oswego, and a Masters of Science in Interactive Media from the University of Central Florida.

View Chris Motola's professional experience on LinkedIn.

Latest posts by Chris Motola (see all)

- Credit Card Company Market Share - March 19, 2024

- Largest Credit Card Networks - March 19, 2024

- The Biggest Credit Card Issuers - March 19, 2024

- Largest Payment Processors - January 17, 2024

- The Complete Guide To ACH Processing Fees - November 30, 2023

To learn more about how we score our reviews, see our Credit Card Processor Rating Criteria.